How to Build Financial Systems Before Scaling

Scaling without financial systems creates cash surprises, weak reporting, and due-diligence failures. Here is how UAE founders and finance leads build the minimum viable finance stack before growth outruns control.

Key takeaways

- Financial systems are the repeatable processes and controls that turn transactions into trustworthy numbers — not just accounting software installed the week before an audit.

- Scale amplifies small weaknesses: delayed bank reconciliation, informal approvals, and one-person bookkeeping become cash crises, tax exposure, and investor red flags.

- Before you scale, you need a clean chart of accounts, monthly close discipline, AR and AP routines, a rolling cash view, and management accounts your leadership team actually uses.

- In the UAE, systems must support VAT records, corporate tax documentation, and bank-ready reporting — authorities and lenders care about evidence, not narratives.

- Hire or outsource selectively: a part-time bookkeeper plus a quarterly review from a qualified accountant often beats an expensive ERP deployed too early.

Growth feels like the goal — more revenue, more customers, more headcount. But scale does not forgive weak finance. It exposes it. The business that wins new contracts without disciplined billing discovers cash trapped in receivables. The team that hires aggressively without a rolling cash view hits payroll week with a surprise. The founder who “will fix the books later” walks into a bank or investor meeting with numbers that do not reconcile — exactly when what investors check before funding a business becomes the only conversation that matters.

Financial systems are how you prevent that. They are the repeatable processes, roles, and controls that turn everyday transactions into numbers you can defend — to your board, your bank, the Federal Tax Authority, and your future self. This guide explains what to build before you scale, in what order, and how UAE founders typically get it wrong. If you are also weighing how to tell that story externally, pair this with how to build an investor-ready financial story in the UAE once the underlying numbers are trustworthy.

What “financial systems” actually means

Founders often hear “systems” and think software. Software matters, but it is only one layer. A workable finance stack has five parts:

- Chart of accounts and coding rules — every transaction lands in a consistent category so reports mean the same thing month to month.

- Transaction capture — sales, purchases, payroll, and expenses are recorded promptly with supporting documents attached.

- Controls — who can spend, who approves, who reconciles the bank, and how exceptions are logged.

- Reporting cadence — monthly close, management accounts, cash forecast, and a short commentary leadership reads.

- Compliance evidence — VAT invoices and returns, corporate tax working papers, contracts, and audit trails stored where you can retrieve them under pressure.

Scale multiplies volume. Systems multiply trust. Without both, you are growing revenue and growing risk at the same time.

None of this requires enterprise complexity on day one. It does require deciding that finance is infrastructure, not admin — the same way you would not scale sales without a CRM. Operators who treat discipline as a growth tool rather than a tax on speed often discover that why compliance is now a growth tool, not just a legal requirement — the same logic applies inside the finance function: clean records accelerate banking, partnerships, and exits.

Why scaling without systems fails

Small businesses can survive informal finance because volume is low and the founder sees every dirham. Scale breaks that visibility. The pattern is predictable, and it is why why cash flow matters more than growth claims in UAE business remains one of the most-read pieces on our Finance desk: growth without cash discipline is a narrative, not an operating model.

Cash surprises

Growth often front-loads cost — people, inventory, marketing, office space — while revenue arrives later. Without AR discipline and a cash forecast, profitable businesses still fail operationally. The failure modes are well documented: 7 cash flow mistakes that put profitable UAE businesses at risk and cash flow mistakes that kill profitable businesses describe the same structural gaps from slightly different angles — delayed invoicing, optimistic forecasts, and confused profit with liquidity.

If investor readiness is on your horizon, weak cash narrative undermines everything else in the room. Why revenue alone does not impress investors is blunt on this point: top-line growth without margin, retention, and cash conversion is a warning sign, not a trophy.

Reporting nobody believes

When accounts are rebuilt before each board pack or tax filing, leadership stops trusting the numbers. Decisions drift to gut feel. Strategic initiatives — new markets, pricing changes, acquisitions — get debated without a shared factual base. That is the difference between why accounting is business intelligence for UAE businesses and treating the ledger as a chore you outsource and forget.

If your team cannot explain variances in plain language, you are not ready to scale headcount or marketing spend. How to read your business numbers before it is too late and the companion how to read business numbers before problems become expensive are practical starting points for founders who did not train as accountants but must still lead with numbers.

Compliance and banking friction

UAE businesses operate inside a mature tax and regulatory environment. VAT requires coherent records. Corporate tax requires defensible positions and documentation. Banks and free-zone authorities ask for statements that tie to reality. Informal spreadsheets at year-end are slower and riskier than monthly discipline — a theme we return to in keeping UAE accounting records ready for tax filing and audit.

If you have recently registered for tax, do not treat registration as the finish line. Corporate tax registration is done: what UAE businesses should do next maps the operating work that follows. On the indirect-tax side, VAT registration in the UAE: when your business should act and voluntary VAT registration in the UAE help you decide timing before scale forces the question under pressure.

Due diligence and exit tax

Buyers and investors do not fund potential; they fund evidence. Due diligence on a fast-scaling company without clean monthly history forces discounts, earn-outs, or walkaways. Building systems early is cheaper than reconstructing two years of books under a data-room deadline — whether you are in traditional sectors or digital assets, where how crypto startups can prepare for due diligence shows how unforgiving evidence standards have become.

If an exit is even remotely on the horizon, systems are how you protect price. How to prepare a business for sale: a practical exit readiness guide and business valuation for SMEs in the UAE both assume you can produce reconciled history — not a heroic reconstruction the month before term sheet.

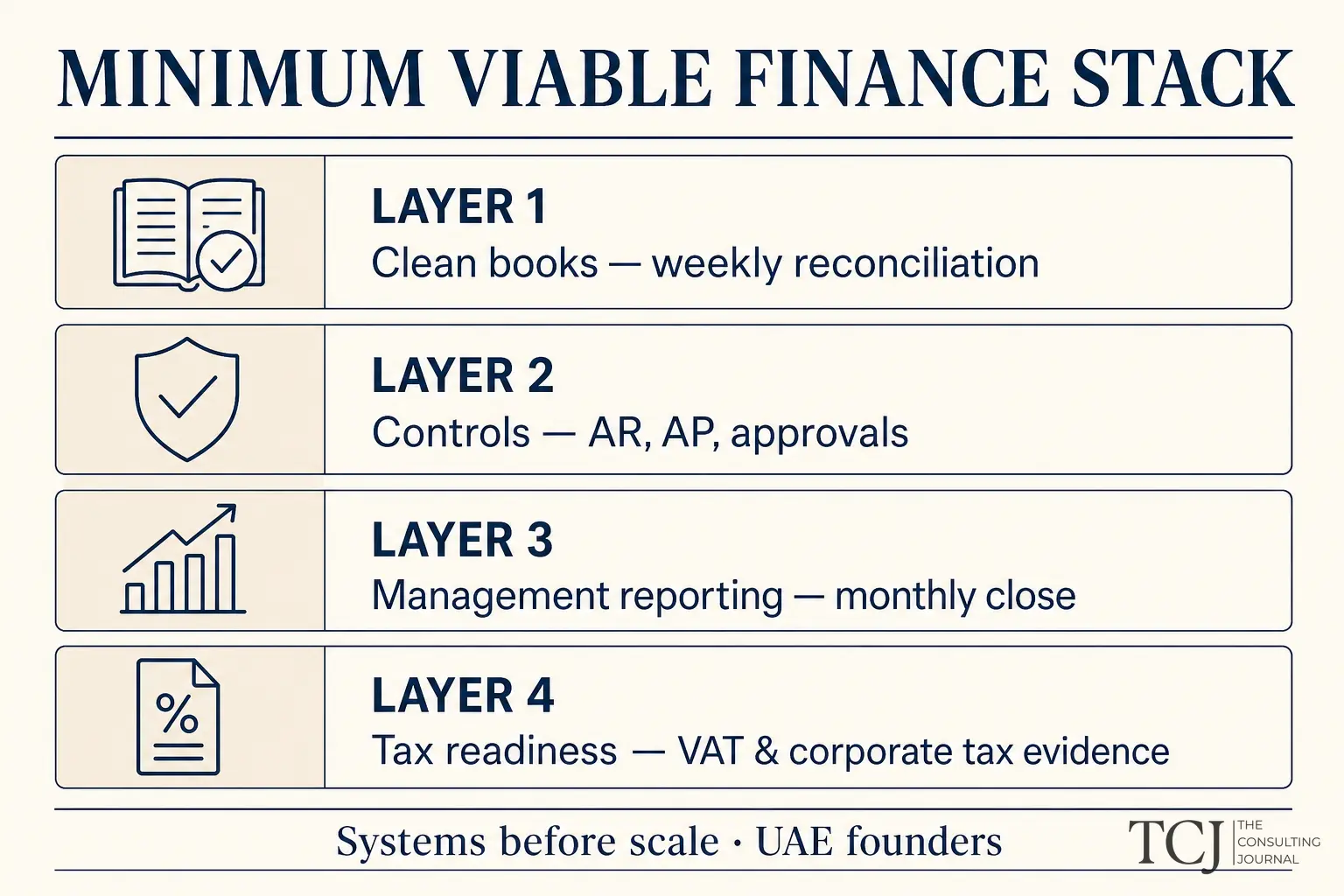

The minimum viable finance stack

Think in layers. Install the layer below before you add headcount or capital that depends on the layer above. This stack is the spine of the article summarised in the header graphic: books → controls → reporting → tax readiness.

Layer 1 — Clean books (weekly rhythm)

- Cloud accounting ledger suited to your entity type and transaction volume.

- Bank feeds reconciled at least weekly — not “when we have time.”

- Sales invoiced promptly; receipts matched to invoices.

- Supplier bills captured with VAT treatment correct at entry, not corrected at filing.

- Document storage: contracts, invoices, receipts, payroll records, bank statements.

If you are still deciding entity structure or activity codes, fix that first — our business setup specialists handle licensing and activity alignment that downstream finance depends on. A wrong activity or jurisdiction choice becomes a recurring tax and banking problem; mainland vs free zone company in the UAE is worth reading before you scale spend.

Layer 2 — Operational controls (monthly rhythm)

- Spend policy — limits by role, required approvals, preferred vendors where practical.

- AR routine — ageing reviewed weekly; chase rules for 30/60/90 days.

- AP routine — payment runs on a schedule; no ad-hoc transfers without a record.

- Payroll checklist — hires, terminations, visa costs, and commissions reflected correctly.

- Inventory or WIP — if applicable, counted or substantiated monthly; do not scale SKUs on guesswork.

Operational systems outside finance still affect the ledger. Why small businesses need systems early argues for documented routines across the business; finance is where those routines show up in cash and compliance.

Layer 3 — Management reporting (monthly close)

Close the books within 5–10 business days of month-end. Leadership should receive:

- P&L vs budget (or prior month if budget is not yet formal).

- Cash in/out summary and runway or covenant headroom.

- Aged AR and AP.

- Three to five bullet variance notes — what moved and what you are doing about it.

Pair this with a practical budget process before growth accelerates. How to build a practical business budget for a growing company is the forward view that makes the P&L actionable. Monthly financial reports every founder should review in the UAE lists the minimum pack — use it as a template until your business needs custom metrics.

Layer 4 — Tax and statutory readiness (quarterly + annual)

- VAT returns filed on time with reconciliations between ledger and return.

- Corporate tax calculations supported by working papers, not intuition.

- Related-party and transfer-pricing documentation if group structures exist.

- Year-end adjustments planned, not invented in March.

Deeper tax posture belongs on the Corporate Tax & Compliance desk. Small business relief in UAE corporate tax may apply to your entity — but relief requires evidence you qualify, not hope. As groups grow, transfer pricing in the UAE: why SMEs should start paying attention explains why intercompany charges belong in your systems early, not after the first audit question.

People, roles, and when to outsource

Systems fail when everything sits with one overloaded person and no backup.

A sensible early-stage split:

| Role | Typical responsibility | |------|------------------------| | Founder / CEO | Approves policy, reviews monthly pack, owns major commitments | | Operations or finance lead | Owns close calendar, AR/AP, cash forecast | | Bookkeeper (in-house or outsourced) | Daily coding, reconciliations, document filing | | Accountant (qualified, periodic) | VAT, corporate tax, year-end, complex judgments |

You do not need a full finance team at fifty employees if routines are clear. You do need named owners and a calendar everyone sees.

Why every business needs CFO thinking for smarter growth is not an argument to hire a full-time CFO on day one. It is an argument that someone must own cash, margin, and capital allocation — even if that person is the founder wearing a second hat. When transaction types multiply, outsourced CFO services in the UAE often bridge the gap between bookkeeping and strategic finance more cheaply than a premature ERP or a hire you cannot keep busy.

When judgments outgrow bookkeeping — multi-currency, inventory, branches, intercompany — engage an accountant before complexity becomes habit. A VAT expert pays for itself the first time you avoid a misclassified supply or a late filing.

Document what you do — policies beat memory

Systems are partly cultural. When only the founder knows how invoices are issued, how refunds are approved, or how petty cash is handled, you do not have a system — you have a dependency. Write one-page policies for:

- Revenue recognition — when you record a sale (invoice date, delivery, milestone) and how you treat deposits.

- Expenses — who can commit spend, receipt requirements, and reimbursement timelines.

- Treasury — which accounts hold operating cash vs tax reserves, and who can initiate transfers.

- Data retention — where contracts and tax invoices live, and for how long.

These documents do not need legal density. They need clarity. Auditors, investors, and new finance hires should be able to follow them without interviewing the founder. If you are building a group structure, align policies with UAE compliance checklist 2026: 21 checks for business owners so statutory obligations have named owners, not orphaned tasks.

How financial systems connect to fundraising and banking

Investors and lenders are pattern-matching machines. They have seen hundreds of decks and thousands of spreadsheets. What separates credible founders is reproducibility: the same revenue definition in January and October, the same EBITDA bridge in the deck and the ledger.

Before you refresh your pitch materials, read investor pitch deck mistakes founders make alongside how to make your business investor-ready before raising capital. Systems are what make those guides actionable instead of aspirational. If you are still choosing between capital sources, debt vs equity financing: which option fits your business growth plan depends on cash visibility you can only get from disciplined reporting.

Banking is the other gate. Scale usually means higher balances, more counterparties, and more scrutiny. Why UAE business bank accounts get rejected is a reminder that financial systems produce the artefacts relationship managers expect — not explanations after the fact. How to build a UAE company banks, tax authorities and clients can trust ties entity design, substance, and records into one narrative.

Forecasting and spend discipline before you scale marketing

One of the most expensive ways to scale is to buy growth before you can measure unit economics. Marketing spend without a forecast is optimism with a invoice attached. Why UAE startups need a financial forecast before marketing spend states the case plainly: systems include a forward view, not only historical reporting.

Automation can help — but only on top of clean data. What UAE businesses can automate and what still needs expert review is a useful filter before you bolt tools onto messy books. AI automation for UAE SMEs: how to cut costs without losing control makes the same point from an operations angle.

A 90-day implementation plan

Days 1–30: Stabilise the foundation

- Audit the chart of accounts; merge unused codes; document coding rules in one page.

- Turn on bank feeds; reconcile all accounts to today.

- List open AR and AP; clear or document disputes.

- Write a one-page spend and approval policy; communicate it.

- Choose a monthly close date (e.g. “books closed by the 7th”).

- Align with the 2026 UAE business checklist: license, tax, VAT, banking, staff and compliance so nothing statutory is orphaned.

Days 31–60: Make reporting routine

- Build a simple budget or quarterly forecast — revenue drivers, fixed costs, hiring plan.

- Produce the first full management pack; note what data was painful to collect; fix that pain.

- Set up VAT checklist: tax invoices, reverse charge, imports/exports if relevant.

- File storage: single folder structure mirrored in cloud and ledger attachments.

- If corporate tax is new to the entity, map your workflow to UAE corporate tax: building a first-year operating system.

Days 61–90: Stress-test before scale

- Run a “mock month-end” in five days instead of fifteen — where are the bottlenecks?

- Update cash forecast using real payment behaviour, not assumptions from launch.

- If fundraising or banking covenants loom, align pack format with what they will ask for.

- Document who covers finance when the primary owner is unavailable.

- Pressure-test valuation narrative with how to increase your business valuation: 17 practical strategies only after the underlying numbers survive basic scrutiny.

Common mistakes founders make

- Buying ERP too early — six months of implementation while invoices still live in email.

- Founder-only approvals — becomes a bottleneck; also hides lack of delegation discipline.

- Confusing revenue with cash — especially on project or subscription businesses with timing gaps.

- No written policies — auditors and investors ask “show me how this works”; memory is not evidence.

- Treating tax as annual — VAT and corporate tax need continuous hygiene; 10 costly corporate tax in UAE mistakes businesses must avoid in 2026 shows how expensive “we will fix it at year-end” becomes.

- Scaling sales before billing discipline — the fastest way to grow AR ageing and customer disputes.

- Ignoring e-invoicing readiness — PDF invoices are not UAE e-invoices explains why format matters as mandates approach; build systems that emit compliant records, not ad-hoc PDFs.

Operators wrestling with growth mechanics more broadly often pair finance discipline with early operating routines — the Ideas desk covers systems thinking outside the ledger, including why execution matters more than motivation in business.

How you know the systems are working

You do not need perfection. You need predictability.

Green signals:

- Month-end close happens on schedule without heroic effort.

- Leadership debates use the same numbers two weeks in a row.

- Cash forecast errors shrink as you learn payment patterns.

- VAT and tax filings do not require rebuilding the ledger.

- Banks and investors receive packs that match what is in the accounting system.

Amber signals — act before scaling hard:

- Frequent “adjustment” journals with vague descriptions.

- AR over 60 days growing faster than revenue.

- No one can explain margin change in one paragraph.

- Payroll costs diverging from headcount records.

If you operate in digital assets as well as traditional revenue, extend the same discipline to on-chain flows — why crypto founders need strong financial reporting is the specialist complement to everything above.

When to upgrade tools — and when to upgrade people

Software upgrades are tempting because they feel like progress. Upgrade when you can name the failure mode: inventory breaks the ledger, multi-entity consolidation takes days, approvals cannot be enforced, or compliance workflows need audit trails the current tool cannot provide. Until then, invest in process and review.

People upgrades follow the same logic. A bookkeeper stops being enough when judgement calls multiply — revenue recognition across contracts, stock valuations, intercompany charges, or tax positions that affect cash. That is the moment to pair operational bookkeeping with periodic strategic review, not to delay until a transaction forces emergency reconstruction. Business valuation for SMEs: how owners can know what their company is worth is easier to act on when the inputs are already clean.

The bottom line

Scaling is not only a sales and product problem. It is a compound interest problem for financial discipline — small gaps become large liabilities when volume rises. Build the minimum viable stack: clean books, basic controls, monthly management reporting, and compliance evidence stored as you go. Use software that fits today’s complexity, not tomorrow’s fantasy architecture. Name owners, run a 90-day implementation, and bring in qualified accounting help when judgments outgrow bookkeeping.

If you want help scoping what “good enough” looks like for your entity before you hire or raise — book a free consultation and we will point you to the right next step. For more on finance, treasury, and balance-sheet decisions, browse the Finance desk and the Investment desk, where capital and reporting meet.

This article is general information for UAE-based businesses and is not legal, tax, or financial advice. Confirm your specific obligations with a qualified adviser before relying on any framework described here.

Questions and answers

What is the difference between financial systems and accounting software?

Accounting software is a tool. Financial systems are the full operating model: who records what, when bank accounts are reconciled, how purchases are approved, how invoices are issued and chased, how often management sees a P&L and cash forecast, and how VAT and corporate tax evidence is stored. Software without routines still produces unreliable numbers.

At what stage should a UAE startup build formal finance systems?

As soon as you have recurring revenue, payroll, or external funding — whichever comes first. If you are hiring, signing leases, or spending marketing budget at scale, you already need monthly closes and cash visibility. Waiting until an investor due-diligence request or your first corporate tax filing is late and expensive to fix.

Do I need an ERP before scaling?

Usually no. Most SMEs scale comfortably on a modern cloud ledger, disciplined processes, and integrated payment and banking feeds. ERPs add cost and complexity; they pay off when transaction volume, inventory, multi-entity structures, or compliance workflows overwhelm simpler tools. Build the habits first, then upgrade software when the pain is specific and measurable.

What reports should leadership review every month?

At minimum: a profit-and-loss statement compared to budget, a cash flow summary or rolling thirteen-week cash view, aged receivables and payables, and a short narrative on variances. Add a balance sheet review once you have debt, inventory, or multiple entities. The goal is decisions, not dashboards nobody opens.

When should I hire an accountant versus keeping bookkeeping in-house?

Bookkeeping can often stay in-house or with a part-time specialist if transactions are routine. Bring in a qualified accountant when you need VAT or corporate tax filings, year-end close, management accounts signed off for investors, payroll complexity, or multi-currency structures. Many UAE businesses use a bookkeeper monthly and an accountant quarterly — that split is efficient if handoffs are documented.

More in Finance

View all Finance →

What UAE Businesses Should Expect From Annual Accounting Services

Annual accounting services should provide reliable year-end records, financial statements, tax preparation support, reconciliations, and practical financial insight. This UAE guide explains reasonable expectations, common exclusions, and how to prepare.

How Long Does It Take to Adjust Financialladjust-financially-moving-dubai

Most newcomers need three to six months to adjust financially after moving to Dubai. Housing, relocation costs, family size and lifestyle choices can make the process shorter or longer.

What's the Real Cost of Dining Out and Entertainment in Dubai in 2026?

A practical 2026 guide to dining, nightlife and entertainment costs in Dubai, with realistic budget ranges, hidden expenses and money-saving advice for visitors, residents and business professionals.