How to Plan Taxes Before Year-End

Year-end tax panic is optional. Here is how UAE founders and finance leads run a structured pre year-end tax review — corporate tax, VAT hygiene, reliefs, and cash provisioning — without crossing into avoidance territory.

Key takeaways

- Tax planning before year-end is about estimating liability, fixing records, and making legitimate timing decisions — not inventing positions after the fact.

- UAE corporate tax requires defensible taxable income calculations supported by working papers; year-end is too late to discover miscategorised revenue or missing related-party documentation.

- VAT hygiene belongs in the same review: ledger-to-return reconciliation, invoice compliance, and reverse-charge treatment prevent painful amendments.

- Small business relief and other elections require evidence you qualify — plan eligibility review before the financial year closes, not at filing.

- Provision cash for tax separately from operating cash; surprise liabilities during growth phases are a common cause of avoidable stress.

Year-end arrives the same way every year — yet many UAE businesses still treat tax as a March surprise. Corporate tax is no longer theoretical. VAT has been operational for years. Banks and investors ask for numbers that tie to filed positions. If your pre year-end routine is “we will fix it when the accountant calls,” you are not planning. You are reconstructing — slowly, expensively, and under pressure.

This guide explains how to plan taxes before year-end in a structured, defensible way: estimates, record hygiene, legitimate elections, cash provisioning, and coordination with your accountant — without drifting into schemes that tax planning vs tax avoidance for UAE business owners warns against.

What “plan before year-end” actually means

Tax planning is not aggressive loophole hunting. For most UAE SMEs it is four practical jobs:

- Estimate corporate tax and VAT exposure with enough accuracy to provision cash.

- Fix categorisation, accruals, and missing documentation while transactions are still current.

- Decide legitimate elections and timing within commercial reality — not artificial arrangements.

- Prepare working papers your accountant can sign — not spreadsheets built in a weekend.

Year-end planning protects cash and credibility. Year-end panic destroys both.

If you recently registered, corporate tax registration is done: what UAE businesses should do next maps ongoing obligations — registration was the starting gun, not the finish line.

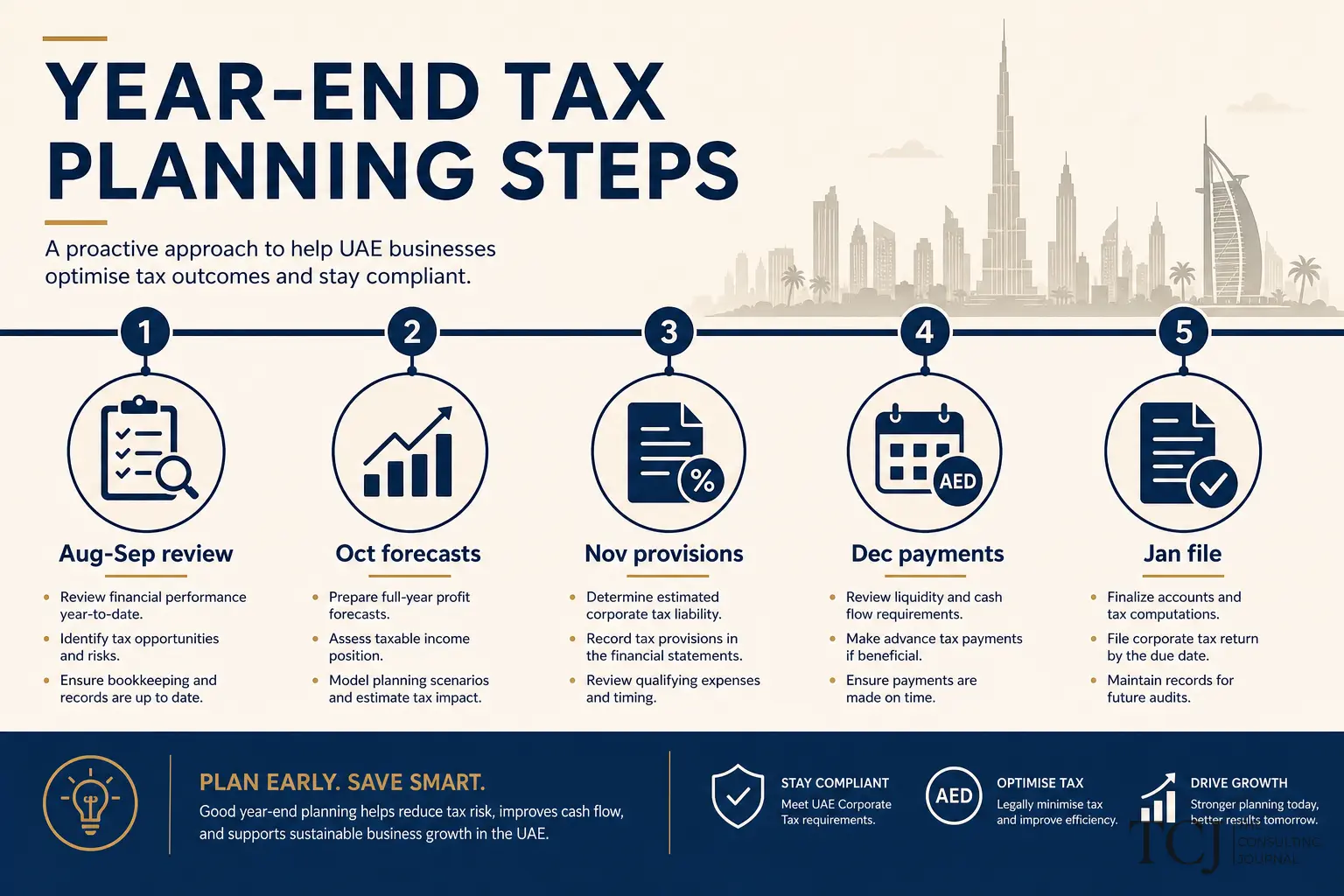

Build the pre year-end calendar

Work backwards from your financial year-end date. Example for a 31 December year-end:

| Timing | Focus | |--------|--------| | T minus 12 weeks | Kickoff: assign owner, request accountant checklist, freeze chart of accounts changes unless necessary | | T minus 8 weeks | VAT reconciliation YTD; fix invoice and coding errors | | T minus 6 weeks | Corporate tax estimate v1; related-party schedule draft | | T minus 4 weeks | Accruals, prepayments, depreciation, inventory/WIP substantiation | | T minus 2 weeks | Management review; cash provision; board or founder sign-off on estimate | | Year-end | Cut-off procedures; lock periods; final adjustments per plan |

Adjust for your year-end — June, March, or free-zone specific dates. The sequence matters more than the label.

Step 1 — Reconcile VAT before you touch corporate tax

VAT errors pollute expense categories and revenue reporting. Start with ledger-to-return reconciliation for each period in the year:

- Output tax on sales matches issued tax invoices.

- Input recovery supported by valid supplier invoices and use tests.

- Reverse charge and imports/exports treated consistently.

- Credit notes and bad debt adjustments documented.

If registration timing was a question earlier in the entity’s life, VAT registration in the UAE: when your business should act remains relevant for amendments and voluntary registration decisions — but year-end is about correctness, not strategy decks.

Common VAT hygiene fixes before close:

- Misclassified exempt vs zero-rated supplies.

- Personal expenses posted with recoverable VAT claimed.

- Missing tax invoices from key suppliers — chase before year-end, not after.

- Point-of-sale or gateway totals not matching ledger revenue.

Clean VAT makes corporate tax estimation trustworthy. Dirty VAT makes every downstream number suspect.

Step 2 — Estimate corporate tax with working papers

Your accountant will compute taxable income — your job is to supply reconcilable inputs:

- Accounting profit per trial balance.

- Adjustments — non-deductible expenses, exempt income, depreciation differences, provisions requiring review.

- Related-party transactions — management fees, royalties, shared costs; documentation per policy.

- Small business relief eligibility — revenue and activity tests per small business relief in UAE corporate tax.

- Loss utilisation — if applicable, track per entity; do not assume cross-entity offsets without structure review.

Avoid corporate tax in UAE mistakes businesses must avoid in 2026: mixing personal and business, missing related-party disclosure, relying on verbal tax “tips,” and booking entries without narrative.

Build estimate v1 at T minus 6 weeks; refresh at T minus 2 after accruals land. Leadership should see a range — base case and conservative case — not a single hopeful number.

Step 3 — Fix the ledger while evidence exists

Year-end adjustments invented without support fail audits. Use the pre year-end window to:

- Accrue known expenses — utilities, bonuses, professional fees, warranty costs.

- Review revenue recognition — milestones, subscriptions, long-term contracts; align with contracts.

- Substantiate inventory and WIP — counts, ageing, obsolescence; impacts both tax and how to read a balance sheet like a business owner.

- Update fixed asset register — additions, disposals, useful lives agreed with accountant.

- Clear stale balances — old accruals, suspense accounts, intercompany differences.

Keeping UAE accounting records ready for tax filing and audit is the standard: if you cannot retrieve the invoice, assume the deduction is at risk.

Software helps when configured correctly — see how to choose accounting software for your business. Garbage in at year-end is still garbage out at filing.

Step 4 — Related-party and group issues

Groups and common founder structures trigger scrutiny on:

- Management charges between entities — basis and agreement.

- Shared staff and cost allocations — defensible drivers.

- Loans between related parties — terms and documentation.

- Transfer pricing for cross-border flows — even SMEs should not ignore intercompany pricing entirely.

If multiple entities exist, planning before year-end includes which transactions close in which period and whether restructuring belongs on the table — always with qualified advice, never DIY memoranda from blog posts.

Step 5 — Legitimate timing decisions — commercial first

Planning may include, where commercially justified:

- Accelerating necessary spend — maintenance, tooling, training — with correct capital vs expense treatment.

- Deferring discretionary bonuses — only with accrual discipline and employee communication ethics.

- Reviewing contracts — milestone billing, deposit structures affecting cash and recognition.

- Elections and reliefs — documented eligibility, not hope.

What planning is not:

- Buying assets you do not need solely for deduction.

- Circular arrangements without substance.

- Personal expenses dressed as business.

- Ignoring VAT recovery rules on “year-end shopping.”

If why businesses fail during growth phases teaches one lesson, it is that cash surprises during expansion hurt — tax-driven spend without cash impact modelling makes that worse.

Step 6 — Provision cash separately

Tax is not operating cash. Set aside:

- Estimated corporate tax payable.

- VAT net payable if periods straddle cash planning.

- Accountant and audit fees for filing season.

Use a separate account or treasury tag if discipline is hard. Pair with how to read a cash flow statement and why cash flow matters more than growth claims in UAE business so tax provisioning appears in leadership’s weekly cash view — not as a single-line shock.

Connect tax planning to management reporting

Tax should not sit in a silo. Pre year-end estimates feed:

- Budget reset — how to build a practical business budget.

- KPIs — effective tax rate and cash tax as metrics in how to create financial KPIs for your company.

- Investor narrative — how to build an investor-ready financial story in the UAE assumes tax is understood, not hand-waved.

- Strategy — why finance should guide strategy, not just reporting includes tax as a constraint on hiring, dividends, and expansion.

Monthly financial reports every founder should review in the UAE should include a rolling tax estimate line once corporate tax applies — not only historical P&L.

Working with your accountant — make the engagement efficient

Bring:

- Reconciled trial balance through latest month.

- VAT reconciliation pack.

- Related-party schedule.

- Fixed asset movement schedule.

- Major contracts list affecting revenue and costs.

- Prior-year computation and correspondence.

- Questions list — elections, relief, uncertain treatments.

Ask explicitly:

- What adjustments do you expect before filing?

- What documentation gaps remain?

- What is our estimated cash payable date?

- What should we change in chart of accounts or process for next year?

Engage a VAT expert or accountant before complexity becomes habit — outsourced CFO services in the UAE can coordinate if internal bandwidth is thin.

Automation and review — what software can and cannot do

AI in accounting for UAE businesses accelerates categorisation and anomaly detection going into year-end — useful for finding miscoded blocks early. It does not replace accountant judgement on tax positions. The future of finance is advisory, automation, and control describes the blend: machines speed prep; humans sign positions.

Pre year-end checklist

- [ ] Owner assigned; accountant checklist received.

- [ ] VAT periods reconciled to ledger; errors corrected.

- [ ] Corporate tax estimate v1 and v2 with narrative adjustments.

- [ ] Related-party transactions scheduled and documented.

- [ ] Small business relief eligibility reviewed with evidence.

- [ ] Accruals, inventory, depreciation, cut-off procedures planned.

- [ ] Cash provision for tax and fees approved.

- [ ] Chart of accounts cleanup completed where agreed.

- [ ] Document retention aligned with UAE accounting records standard.

- [ ] Board or founder review of estimate and risks.

Year-end planning and investor or lender timelines

If fundraising or facility renewal overlaps your year-end, tax planning and external narrative must align. What investors check before funding a business includes tax liabilities, provisions, and related-party exposure — surprises in the data room erode trust faster than a soft quarter. Why revenue alone does not impress investors extends to tax quality: aggressive positions without documentation signal governance risk.

increase business valuation strategies work when earnings are “clean” — normalised adjustments documented, not invented at sale. Pre year-end is when you remove one-offs from run-rate earnings or document them clearly as non-recurring, rather than letting investors discover ambiguous journals later.

investor pitch deck mistakes founders make include showing EBITDA without reconciling tax cash — plan both in the same review.

Systems and ownership — tax is not only accountant work

Why small businesses need systems early applies to tax operations: coding rules, document capture, approval trails. Why every business needs CFO thinking for smarter growth means someone internal owns the calendar — chasing documents, reconciling VAT, ensuring accruals land — even when filing is outsourced.

Weak internal ownership produces year-end archaeology. Strong ownership produces estimates leadership trusts for hiring and dividend decisions in Q4.

Common pre year-end mistakes

- Starting too late — no time to fix evidence gaps.

- Single-point estimate — no range, no cash plan.

- VAT ignored until corporate tax done — polluted inputs.

- Personal/business blur — expensive on audit.

- Undocumented related-party flows — slow filings, slow due diligence.

- Shopping for deductions — cash out, benefit uncertain.

- Assuming software “handled tax” — it recorded transactions; you still own positions.

Link operational finance to systems: build financial systems before scaling and why accounting is business intelligence for UAE businesses reduce year-end fire drills when routines run monthly.

Coordinating accountant, auditor, and internal team

Pre year-end planning fails when external advisers receive chaotic handoffs. Assign one internal owner to the data room — even if part-time — who maintains:

- Rolling trial balance notes on unusual balances.

- VAT reconciliation files per period.

- Related-party transaction log updated when deals occur, not in December.

- Cap table and dividend or distribution records if relevant.

Your accountant should receive the same pack monthly in lighter form — surprises shrink when advisers see trends before year-end peak. Engage outsourced CFO services in the UAE or a qualified accountant early if internal bandwidth cannot own the calendar.

Auditors and tax authorities ask “show the working” — AI in accounting for UAE businesses speeds preparation but does not replace organised evidence.

After year-end — carry learnings forward

Close the loop with a one-page “tax operating memo” for next year: what broke, what to automate, which accounts need coding rules, when to refresh estimates. Feed that memo into build financial systems before scaling and software choices in how to choose accounting software for your business.

Planning taxes before year-end is not an annual event — it is the sharp end of a monthly discipline that includes monthly financial reports every founder should review in the UAE and cash provisioning visible in how to read a cash flow statement.

The bottom line

Planning taxes before year-end is disciplined estimation, record repair, legitimate elections, and cash provisioning — executed on a calendar with your accountant, not in a panic after the period closes. Reconcile VAT first, estimate corporate tax with working papers, substantiate balance sheet items, document related-party flows, and provision cash separately from operations.

Done well, year-end becomes confirmation — not archaeology. Done poorly, it becomes the tax and cash crisis that why businesses fail during growth phases warns about.

For help scoping your pre year-end review, book a free consultation. Browse Corporate Tax & Compliance and the Finance desk for related guides.

This article is general information for UAE-based businesses and is not legal, tax, or financial advice. Confirm your specific obligations with a qualified tax adviser before relying on any framework described here.

Questions and answers

When should UAE businesses start year-end tax planning?

At least eight to twelve weeks before your financial year-end, earlier if you have inventory, related-party transactions, or multi-entity structures. You need time to reconcile VAT, estimate corporate tax, accrue adjustments, gather documentation, and fix categorisation errors without rushing journals that auditors and the Federal Tax Authority will question.

What is the difference between tax planning and tax avoidance in the UAE?

Planning uses legitimate structures, elections, and timing within the law — supported by substance and records. Avoidance schemes rely on artificial arrangements with little commercial purpose and often collapse under scrutiny. Tax planning vs tax avoidance for UAE business owners covers the line in detail; if a strategy cannot be explained plainly to an auditor, treat it as high risk.

Does small business relief apply automatically?

No. Relief depends on meeting eligibility conditions and maintaining evidence. Review revenue thresholds, entity structure, and excluded activities with your accountant before year-end. Small business relief in UAE corporate tax explains the framework — qualification is factual, not aspirational.

What documents should be ready before year-end close?

At minimum: reconciled trial balance, VAT return reconciliations for the year, related-party transaction schedules, fixed asset register, loan agreements, major contracts affecting revenue recognition, stock counts or WIP substantiation, and prior-year tax computations if applicable. Keeping UAE accounting records ready for tax filing and audit is the operating standard.

Should I make large purchases before year-end to reduce tax?

Only when commercially justified and when the tax treatment matches your assumptions. Accelerating spend for deduction alone can hurt cash without benefit if the expense is capitalised, not deductible as assumed, or paid but not yet incurred under accrual rules. Model the impact with your accountant — do not shop your way out of planning.

More in Finance

View all Finance →

What UAE Businesses Should Expect From Annual Accounting Services

Annual accounting services should provide reliable year-end records, financial statements, tax preparation support, reconciliations, and practical financial insight. This UAE guide explains reasonable expectations, common exclusions, and how to prepare.

How Long Does It Take to Adjust Financialladjust-financially-moving-dubai

Most newcomers need three to six months to adjust financially after moving to Dubai. Housing, relocation costs, family size and lifestyle choices can make the process shorter or longer.

What's the Real Cost of Dining Out and Entertainment in Dubai in 2026?

A practical 2026 guide to dining, nightlife and entertainment costs in Dubai, with realistic budget ranges, hidden expenses and money-saving advice for visitors, residents and business professionals.