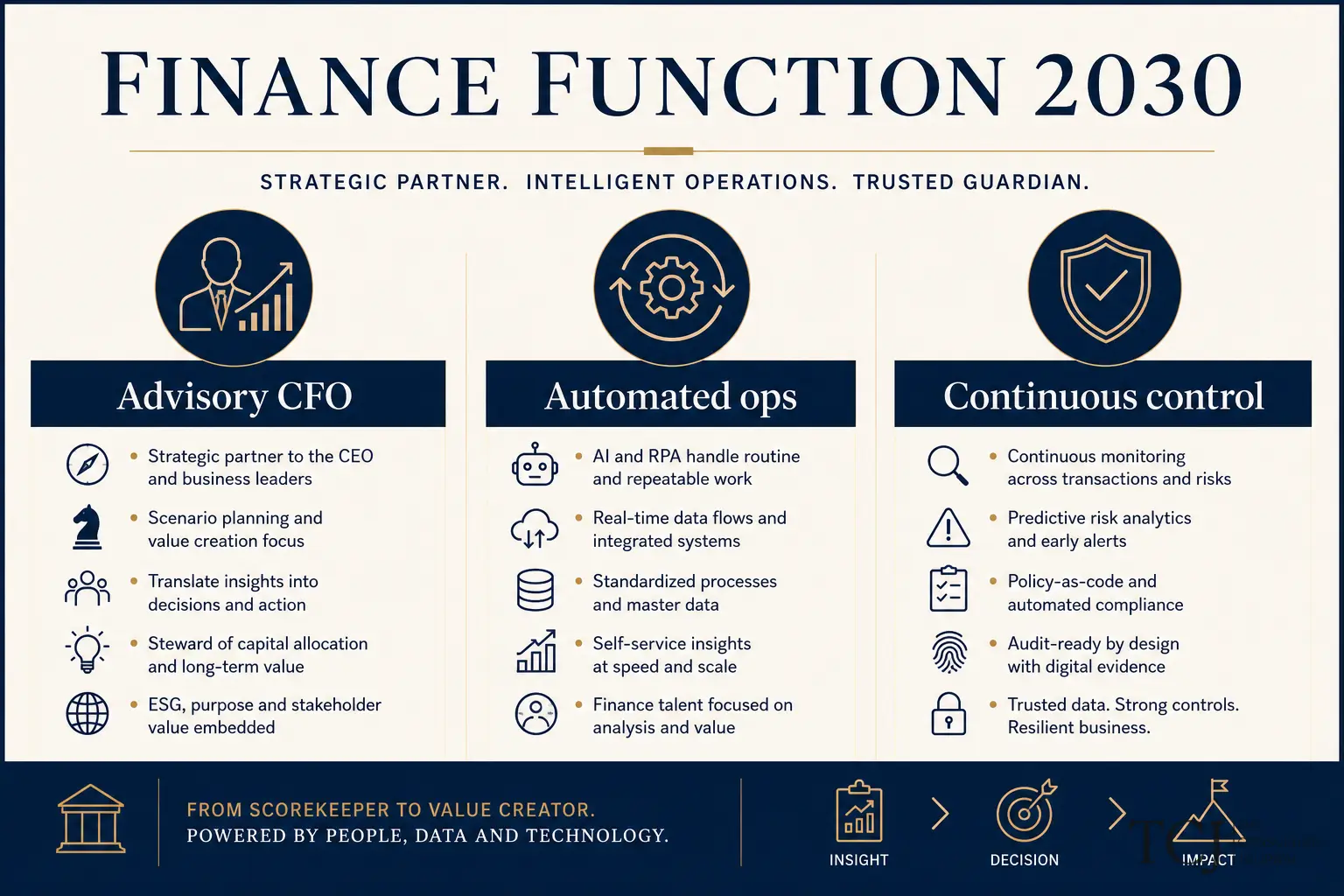

The Future of Finance Is Advisory, Automation, and Control

Finance teams in UAE SMEs will spend less time on manual entry and more on judgment, scenario planning, and controls — if they automate on clean data. Here is what advisory, automation, and control mean in practice for founders and finance leads.

Key takeaways

- The future of finance is not humans vs machines — it is advisors using automation to produce faster, cleaner numbers while focusing judgment on tax, capital, and strategy.

- Automation without control creates speed and errors at scale; control without automation burns talent on tasks that software should handle.

- UAE businesses face rising compliance depth — VAT, corporate tax, e-invoicing pressure — automation helps evidence; advisers sign positions.

- Founders should invest in data hygiene and integration first, then layer automation — not bolt AI onto messy ledgers.

- Outsourced and fractional models will grow: bookkeepers plus automated feeds plus periodic CFO review — full in-house teams where complexity justifies.

Finance is undergoing a structural shift — not the dramatic “robots replace CFOs” headline, but a quieter reorganisation of work. Repetitive capture, matching, and reporting compress into minutes through automation. Compliance demands more evidence, faster. Founders expect numbers in near real time for hiring and spend calls. Meanwhile, judgment calls — tax positions, capital allocation, pricing trade-offs, fraud and error detection — matter more, not less, because speed amplifies mistakes as easily as efficiency.

The future of finance for UAE businesses is advisory, automation, and control working as one system: machines handle volume; controls enforce trust; advisers — internal or external — interpret signals and guide strategy. This article explains what that model means in practice, how to build toward it without hype, and where founders and finance leads should invest first.

The three pillars defined

Advisory

Finance as decision partner — not only compliance output:

- Scenario planning and budget refresh — how to build a practical business budget.

- KPI design and variance coaching — how to create financial KPIs for your company.

- Tax and structure guidance — how to plan taxes before year-end, tax planning vs tax avoidance.

- Fundraise and investor narrative — how to build an investor-ready financial story in the UAE.

Why finance should guide strategy, not just reporting is the cultural frame; advisory is the job description.

Automation

Software and rules executing high-volume, repeatable work:

- Bank transaction matching and coding suggestions.

- Recurring journals and depreciation runs.

- Receipt OCR with human exception queues.

- Automated management packs from closed periods.

- Anomaly flags — duplicate vendors, unusual amounts, period-over-period spikes.

AI in accounting for UAE businesses: automation and expert review separates what to automate from what still needs qualified eyes.

Control

Governance that keeps automated speed trustworthy:

- Role-based access and approval workflows.

- Segregation between recorder and reconciler.

- Locked accounting periods after close.

- Document retention aligned with keeping UAE accounting records ready for tax filing and audit.

- Policies for revenue recognition, spend, and treasury — written, not tribal.

Automation scales your process — including your weaknesses. Control is what makes speed safe.

Build financial systems before scaling — control is layer two of the stack.

Why this model fits the UAE now

Corporate tax — continuous categorisation and documentation; year-end heroics fail under scrutiny — corporate tax mistakes to avoid in 2026.

VAT maturity — reconciliation automation reduces filing errors; advisers interpret complex supplies — VAT registration when to act.

Banking and investor scrutiny — reproducible numbers from integrated systems — what investors check before funding a business.

SME talent constraints — founders cannot manually code five hundred transactions while leading sales; automation preserves advisory bandwidth for why every business needs CFO thinking.

Growth risk — why businesses fail during growth phases when control does not scale with volume.

The target operating model — how work flows

- Capture — invoices, bank feeds, payroll, expenses flow into ledger via integrations chosen in how to choose accounting software for your business.

- Automate — rules match, categorise, flag exceptions for review.

- Control — approvals on spend, vendor changes, journal entries above threshold; monthly close checklist.

- Report — P&L, balance sheet, cash, KPIs — how to read a profit and loss statement, balance sheet, cash flow.

- Advise — leadership meeting: variances, scenarios, decisions logged.

- Comply — VAT and corporate tax filings with working papers; small business relief reviewed with evidence.

Broken capture cannot be fixed by better advisory — garbage in, automated garbage out.

What to automate first — practical sequence

Phase 1 — Foundation (weeks 1–4)

- Cloud ledger with bank feeds.

- Chart of accounts cleanup.

- Document attachment habit.

- Weekly reconciliation.

Phase 2 — Volume (weeks 5–12)

- Receipt capture with review queue.

- Recurring transaction rules.

- AR/AP ageing automated reports.

- Standard monthly pack template — monthly financial reports for founders.

Phase 3 — Intelligence (months 4–6)

- Anomaly detection on spend and coding.

- Cash forecast linked to ledger actuals.

- KPI dashboard auto-populated post-close.

Phase 4 — Advisory uplift

- Scenario models for hire/spend decisions.

- Quarterly tax estimate refresh.

- Board or investor pack automation from single source.

Do not skip phases — why small businesses need systems early.

What stays human — non-negotiable advisory

- Revenue recognition judgments across contracts.

- Related-party pricing and documentation.

- Corporate tax positions and elections — corporate tax registration next steps.

- Fraud investigation and control design.

- Capital structure and fundraise terms — investor pitch deck mistakes.

- Explaining variances that drive strategy — margin, cash, working capital — why cash flow matters more than growth claims.

Automation proposes; advisers dispose — especially where why revenue alone does not impress investors and quality of earnings matter.

Control in an automated environment — new risks

Speed without gates creates:

- Mass miscoding before anyone notices.

- Duplicate payments cleared by volume.

- Period lock bypassed for “quick fixes.”

- AI-suggested entries accepted without review.

Mitigations:

- Exception queues with SLAs.

- Sample-based review even when automation rate is high.

- Change logs on master data — vendors, bank details, COA.

- Dual approval on sensitive master data changes.

Why accounting is business intelligence for UAE businesses requires trustworthy inputs — control delivers that.

Organisation models — who does what

| Role | Future focus | |------|----------------| | Founder / CEO | Strategy, approvals, capital calls; reads KPI pack | | Finance lead / fractional CFO | Advisory, scenarios, tax coordination, control design | | Bookkeeper / ops finance | Exception handling, close execution, document chase | | Accountant (qualified) | Tax sign-off, complex judgments, filing | | Software + automation | Matching, recurring tasks, standard reports |

Outsourced CFO services in the UAE — hybrid model grows because it maps cleanly to this split.

Full in-house teams make sense when entity count, transaction complexity, and fundraising cadence exceed fractional capacity — not when a founder buys ERP to avoid hiring discipline.

Technology choices — platform not point solutions

Prefer:

- Integrated ledger as hub — choose accounting software.

- Fewer bolt-ons with duplicate data.

- API-stable vendors with export rights.

Avoid:

- AI wrappers on parallel spreadsheets.

- Automation that bypasses the ledger.

- Tools that cannot produce audit trail.

increase business valuation strategies — buyers trust single source of truth.

Measuring progress — maturity indicators

Level 1 — Manual: Spreadsheets, delayed close, reactive tax.

Level 2 — Digitised: Cloud ledger, bank feeds, monthly close on calendar.

Level 3 — Automated: Rules, capture tools, exception queues, KPI automation.

Level 4 — Advisory-led: Scenarios drive decisions; tax modelled forward; controls tested.

Most UAE SMEs should aim for Level 3 with selective Level 4 capability — not Level 4 theatre with Level 1 data.

Risks and honest limits

- Vendor hype — “AI closes your books” — no, it assists.

- Compliance outsourcing without ownership — you still sign filings.

- Automation before COA discipline — accelerates chaos.

- Cost creep — twelve SaaS tools replacing one hire — model TCO.

- Cyber and access — more integrations, more attack surface — role permissions matter.

Tax planning vs tax avoidance — automation does not legitimise aggressive schemes.

Connecting to the rest of your finance stack

This future state integrates guides across the desk:

- Systems — build financial systems before scaling.

- Reading statements — P&L, balance sheet, cash flow.

- KPIs and strategy — financial KPIs, finance guides strategy.

- Growth discipline — why businesses fail during growth phases.

The future is not a product you buy — it is an operating model you build.

Change management — people adopt the model

Automation fails when bookkeepers fear replacement or founders bypass controls “just this once.” Communicate clearly: automation removes re-keying; advisers interpret; owners still approve. Train on exception queues — the job shifts from typing to reviewing — often higher value and less burnout.

Document policies when automation enforces them — approval limits, vendor onboarding, period lock rules. Why accounting is business intelligence for UAE businesses requires people to trust outputs; training builds trust.

Twelve-month roadmap summary

| Quarter | Focus | |---------|--------| | Q1 | Ledger hygiene, bank feeds, weekly rec, COA cleanup | | Q2 | Capture automation, close calendar, KPI pack v1 | | Q3 | Control hardening, tax integration, cash forecast automation | | Q4 | Advisory scenarios, investor/bank pack, tool upgrade if named pain |

Revisit build financial systems before scaling each quarter — systems are living infrastructure.

Vendor selection — automation with control built in

When choosing capture, AP automation, or reporting tools, score vendors on:

- Audit trail completeness — who changed what, when.

- Role permissions granularity.

- Export and exit — data portability if you leave.

- Integration with your ledger — how to choose accounting software for your business as hub.

- Exception workflow — not black-box AI posting without review queue.

Prefer vendors whose automation respects period locks and approval matrices — control-native, not control-bolted-on.

Fractional vs in-house — advisory capacity planning

Map headcount to complexity:

- Under ~50 transactions/day, single entity: bookkeeper + automation + quarterly accountant often suffices.

- Multi-entity, inventory, fundraising: add fractional CFO or finance lead for advisory layer.

- Regulated, multi-country, high audit exposure: in-house finance team with external tax specialists.

Outsourced CFO services in the UAE scale advisory without fixed CFO cost — automation reduces hours spent on capture so fractional time goes to scenarios and tax coordination per how to plan taxes before year-end.

Security, access, and continuity

Automation increases integration surface — bank feeds, payroll APIs, expense tools. Finance must own:

- Access reviews when staff leave — remove permissions same day.

- Two-factor authentication on ledger and banking.

- Backup of policies and chart of accounts documentation outside single person’s laptop.

- Continuity plan — who closes month if primary finance owner is unavailable per build financial systems before scaling.

Control includes cyber hygiene — not only approval workflows.

Measuring ROI on finance transformation

Track before/after:

- Days to close month-end.

- Hours spent on bank rec and coding.

- Forecast error band width.

- Tax adjustment count at year-end.

- AR days trend.

ROI is time returned to advisory work and error reduction — not only software subscription cost. Pair with how to create financial KPIs for your company so transformation metrics survive past project launch.

Working with regulators and auditors in an automated world

FTA and audit expectations remain evidence-based — automation must produce retrievable audit trails, not opaque black boxes. When implementing AI categorisation, retain human approval logs and model change history. Keeping UAE accounting records ready for tax filing and audit standards apply regardless of tooling fashion.

Auditors may sample automated entries more heavily early in adoption — expect that scrutiny and welcome it as validation of control design. Advisory finance prepares narrative for auditors; automation supplies population data; control framework connects both.

When evaluating new automation, pilot on one entity or one bank account first — prove control and accuracy before enterprise rollout. Pilots surface coding rule gaps cheaply; big-bang rollouts surface them expensively under month-end pressure.

The UAE finance function of 2026 is neither fully manual nor fully autonomous — it is a hybrid where advisers set policy, software executes volume, and controls prove trust to FTA, banks, and boards. Build toward that hybrid deliberately rather than buying tools without process.

Measure progress quarterly — close days, rec hours, forecast error — and adjust the roadmap. Transformation without metrics becomes vendor shopping; metrics keep advisory, automation, and control aligned to outcomes.

The bottom line

The future of finance is advisory, automation, and control — advisers focusing on judgment and strategy, automation handling volume on clean data, and controls ensuring speed does not erode trust. UAE businesses face compliance and growth pressure that manual finance alone cannot sustain affordably — but automation on messy process only fails faster.

Start where you are: stabilise the ledger, automate capture and matching, harden controls, then expand advisory capacity — internal or fractional — as complexity grows. The businesses that win the next decade will not have the most transactions typed manually; they will have the clearest numbers, fastest close, and best decisions per dirham of finance cost.

For help scoping your finance automation and advisory roadmap, book a free consultation. Browse the Finance desk for related guides on how to choose accounting software for your business, why finance should guide strategy, not just reporting, and the full reporting trilogy.

This article is general information for UAE-based businesses and is not legal, tax, or financial advice. Confirm your specific obligations with a qualified adviser before relying on any framework described here.

Questions and answers

Will automation replace accountants in the UAE?

Automation replaces repetitive tasks — matching, coding suggestions, reconciliation flags, report generation — not professional judgment on tax positions, related-party transactions, revenue recognition, or audit defence. Demand shifts toward advisers who interpret automated outputs and guide strategy — see why finance should guide strategy, not just reporting.

What finance tasks should UAE SMEs automate first?

Bank feed matching, recurring entries, receipt capture with review queues, aged AR/AP reports, standard management packs, and VAT reconciliation worksheets fed from the ledger. Automate high-volume, rules-based work first; keep expert review on exceptions, tax classifications, and year-end adjustments per AI in accounting for UAE businesses.

What does control mean in modern finance?

Control means defined owners, approval workflows, segregation of duties, audit trails, locked periods, documented policies, and monitoring — whether transactions are entered manually or by automation. Growth without control is why why businesses fail during growth phases resonates: volume exposes weak gates.

How should founders balance automation cost vs hiring?

Compare fully loaded hire cost to software plus fractional advisory for the same output — often hybrid wins early. Automate capture and reconciliation; hire or outsource judgment on close, tax, and strategy. Outsourced CFO services in the UAE exemplify the blend.

Is the future of finance relevant to small UAE businesses?

Especially relevant. Corporate tax and digital reporting raise the bar for evidence and timeliness — small teams cannot absorb volume with manual process alone. Advisory-automation-control is how SMEs keep bank-grade records without bank-grade headcount — if built on financial systems before scaling.

More in Finance

View all Finance →

What UAE Businesses Should Expect From Annual Accounting Services

Annual accounting services should provide reliable year-end records, financial statements, tax preparation support, reconciliations, and practical financial insight. This UAE guide explains reasonable expectations, common exclusions, and how to prepare.

How Long Does It Take to Adjust Financialladjust-financially-moving-dubai

Most newcomers need three to six months to adjust financially after moving to Dubai. Housing, relocation costs, family size and lifestyle choices can make the process shorter or longer.

What's the Real Cost of Dining Out and Entertainment in Dubai in 2026?

A practical 2026 guide to dining, nightlife and entertainment costs in Dubai, with realistic budget ranges, hidden expenses and money-saving advice for visitors, residents and business professionals.