How to Read a Profit and Loss Statement

The P&L tells you whether the business model works — if you know which lines matter. Here is a practical guide for UAE founders and operators to read a profit and loss statement for decisions, not decoration.

Key takeaways

- A profit and loss statement measures performance over a period — not cash in the bank or balance sheet strength.

- Gross margin is the first test of business model viability; operating expenses only matter after you understand unit economics at the top of the P&L.

- Compare P&L to budget and prior periods with a short variance narrative — numbers without explanation rarely change behaviour.

- Revenue definition must be consistent month to month; changing recognition rules mid-stream destroys trust with investors and your own team.

- Pair the P&L with cash flow and balance sheet review monthly — profit alone misleads during growth.

Most founders can quote revenue from memory. Fewer can explain why gross margin moved three points last month, which operating line absorbed a hiring decision, or whether net profit included a one-off that will not repeat. That gap matters — because the profit and loss statement is where the business model proves itself. Not in the pitch deck. Not in the CRM pipeline. In the ledger, month after month, with definitions stable enough that your team and your bank believe the same story.

This guide shows how to read a profit and loss statement as an operator: what each section means, which lines to scrutinise first, how to compare periods without drowning in spreadsheets, and how the P&L connects to cash and the balance sheet in a UAE context. If you are building the habit from scratch, pair this with monthly financial reports every founder should review in the UAE.

What a P&L is — and what it is not

The profit and loss statement — income statement, statement of comprehensive income — summarises revenue, costs, and profit over a period (a month, quarter, or year). It answers: did we sell enough, at the right price, with controlled delivery cost and overhead, to leave something for tax and reinvestment?

It is not:

- A cash report — see how to read a cash flow statement.

- A snapshot of what you own and owe — see how to read a balance sheet like a business owner.

- A substitute for unit economics — the P&L consolidates; you still need segment views.

Revenue is the headline. Gross margin is the verdict. Net profit is the footnote until you understand the first two.

Why accounting is business intelligence for UAE businesses treats the P&L as a decision tool — not filing output.

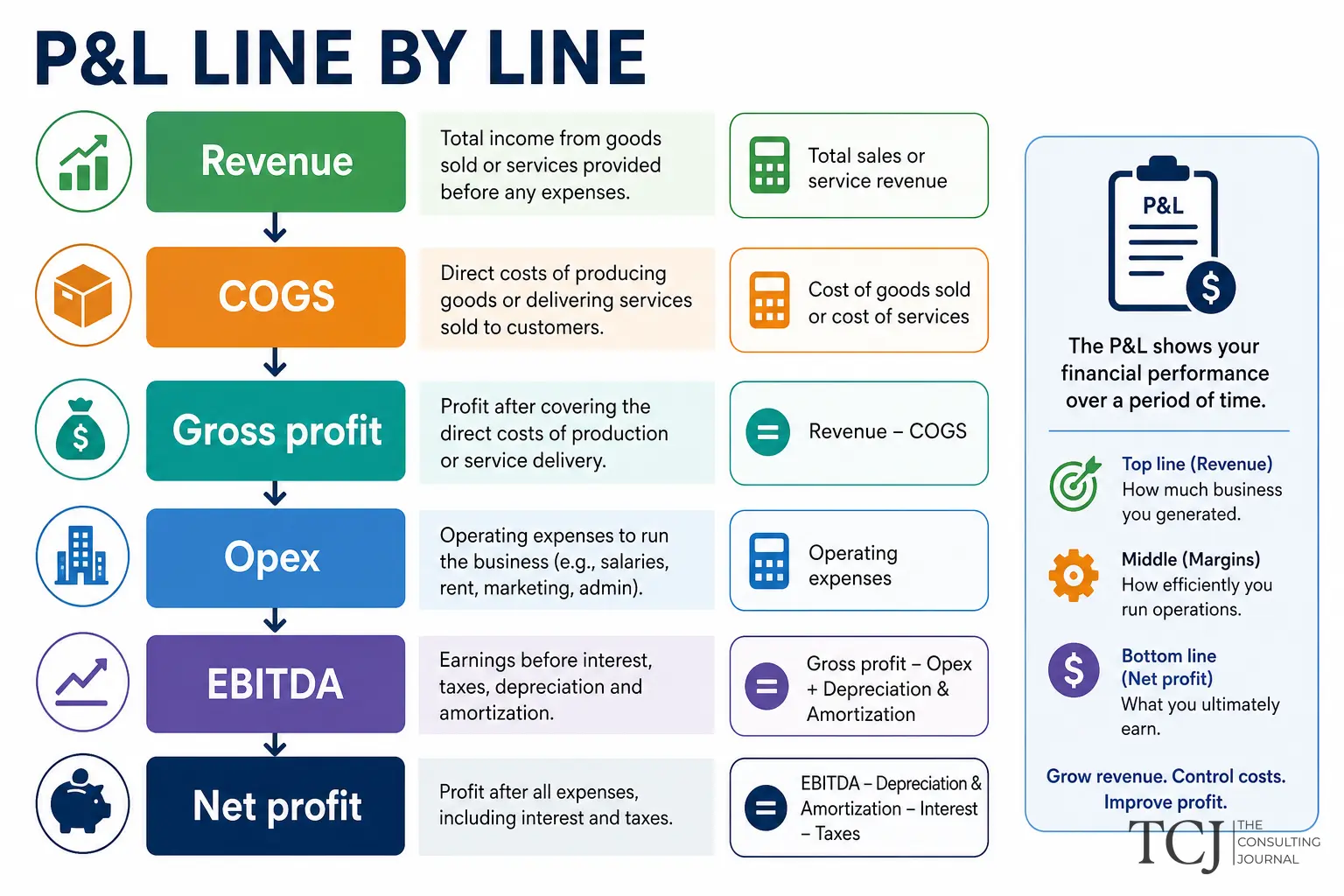

Anatomy of a standard P&L

Typical structure top to bottom:

Revenue (turnover)

All income from core activities — sales of goods, services, subscriptions, project fees — net of returns and discounts, per your accounting policy. VAT collected is usually excluded from revenue; it is a balance sheet liability until remitted.

Founder questions:

- Is revenue broken down by stream, product, or geography we actually manage?

- Are we consistent on when we recognise revenue — invoice, delivery, milestone?

- Do gateway or marketplace fees net against revenue or sit in expenses — and is that consistent?

Inconsistency here breaks investor trust — why revenue alone does not impress investors and what investors check before funding a business both assume definitional stability.

Cost of goods sold (COGS) / cost of sales

Direct costs to deliver what you sold: materials, subcontractor delivery, shipping on goods, payment processing tied to sales, stock consumed. For pure services, this may be delivery payroll or contractor cost allocated to projects.

Founder questions:

- What belongs in COGS vs operating expenses — and is coding stable?

- If margin dropped, was it price, mix, or delivery cost?

- For inventory businesses, did COGS reflect an accurate count?

Gross profit and gross margin

Gross profit = Revenue − COGS

Gross margin % = Gross profit ÷ Revenue

This is the first viability test. A business can survive weak net profit temporarily with tight opex; sustained weak gross margin usually means pricing, product, or delivery model failure — not “we will fix it with volume.”

Track gross margin monthly and vs how to build a practical business budget. During growth, why businesses fail during growth phases often traces back to margin erosion hidden by rising revenue.

Operating expenses (OPEX)

Indirect costs to run the business: sales and marketing, general admin, rent, software, professional fees, management salaries not charged to COGS, depreciation of operating assets.

Subcategories vary by chart of accounts. What matters is materiality — list the five largest opex lines and own an owner for each.

Founder questions:

- Which costs are fixed vs variable with headcount or revenue?

- Did marketing spend produce measurable pipeline or revenue — or just activity?

- Are personal or non-deductible items isolated for tax clarity per how to plan taxes before year-end?

Operating profit (EBIT or similar)

Profit after COGS and operating expenses, before interest and tax. Some packs show EBITDA — before depreciation and amortisation too. Useful for comparing operating performance when capital structure differs; misleading if you ignore capex-heavy reality.

Finance costs and other income/expense

Interest on loans, bank charges, FX gains/losses, asset disposals, one-off legal settlements. Separate these mentally from recurring operating performance — investors and how to build an investor-ready financial story in the UAE want recurring vs non-recurring split clearly.

Tax and net profit

Corporate tax provision (estimated or actual) and net profit after tax. In UAE corporate tax era, treat tax as a real operating planning line — not a surprise line in month twelve. Corporate tax in UAE mistakes businesses must avoid in 2026 includes treating tax as someone else’s problem until filing.

How to read a P&L in thirty minutes each month

Step 1 — Flash the headline (five minutes)

- Revenue vs budget and vs last month / last year same month.

- Gross margin % — flag if move exceeds your materiality threshold (often 1–2 points).

- Net profit — note one-offs before reacting.

Step 2 — Variance narrative (fifteen minutes)

For each material movement, one sentence:

- What moved? (volume, price, mix, cost rate, timing)

- Why? (contract, campaign, hire, supplier, seasonality)

- Action? (hold, fix, investigate, ignore as one-off)

If you cannot write the sentence, your chart of accounts or coding discipline needs work — not another dashboard. How to choose accounting software for your business and build financial systems before scaling address upstream fixes.

Step 3 — Connect to cash and balance sheet (ten minutes)

- Did revenue growth increase AR faster than cash collected?

- Did profit include accruals without cash yet — bonuses, supplier terms?

- Any large prepayments or deferred revenue on the balance sheet affecting next month’s P&L?

Why cash flow matters more than growth claims in UAE business exists because founders stop at net profit. Do not.

Comparisons that actually help

| Comparison | Purpose | |------------|---------| | vs Budget | Accountability to plan — practical business budget | | vs Prior month | Operational pulse — seasonality and campaign effects | | vs Same month prior year | Growth and margin trend — removes some seasonality | | vs KPI targets | Links P&L to financial KPIs |

Avoid comparing P&L to bank balance directly — use cash flow statement instead.

Segment and unit views — where truth hides

Consolidated P&L flatters bad products and punishes good ones in silence. Where possible, review:

- By product line or service type.

- By customer segment or channel.

- By project or contract type for agencies.

- Contribution margin after direct variable costs.

You may need management accounts beyond statutory format — outsourced CFO services in the UAE often build these views on top of the ledger.

P&L discipline and early-stage systems

You do not need a finance team to read a P&L monthly — you need a closed ledger and twenty minutes of focus. Early-stage operators sometimes defer formal reporting until “we are big enough.” That delay trains bad coding habits and hides margin problems until headcount is already committed. Why small businesses need systems early includes choosing revenue recognition rules before volume makes retroactive fixes painful.

Pair first monthly P&L reviews with a simple budget — how to build a practical business budget for a growing company — so “vs budget” means something on line one.

Tax lines on the P&L — corporate context

Once corporate tax applies, isolate estimated tax charge or provision in management view even if your accountant finalises the computation later. Founders surprised by tax on profit often failed to watch provision build through the year — corporate tax registration is done: what UAE businesses should do next is the starting point for ongoing estimates, not only registration paperwork.

Review whether small business relief in UAE corporate tax affects your run-rate tax assumption — relief changes effective rate and cash planning when eligible.

On planning posture, tax planning vs tax avoidance for UAE business owners reminds you that P&L optimisation must stay within defensible commercial substance — aggressive “adjustments” without documentation show up painfully in audit and diligence.

Common P&L mistakes founders make

- Celebrating revenue without margin — volume on unprofitable SKUs.

- Ignoring mix shift — average price up, but low-margin product grew faster.

- Capitalising what should expense — inflates profit temporarily.

- Inconsistent revenue recognition — month-end sales stuffed or deferred informally.

- Blending personal and business — distorts every ratio.

- One spreadsheet for management, another for tax — divergence under due diligence.

- Reading P&L without AR ageing — profit without collection is narrative.

Investor pitch deck mistakes founders make often start when deck EBITDA ≠ ledger EBITDA.

P&L and UAE compliance context

VAT does not belong in revenue, but VAT treatment affects recoverable input on COGS and opex — miscoding shows up as margin noise and tax risk. Keeping UAE accounting records ready for tax filing and audit and VAT registration in the UAE sit alongside monthly P&L review, not instead of it.

Corporate tax makes non-deductible expenses worth isolating in management view — entertainment limits, fines, certain provisions — so estimates in how to plan taxes before year-end are not rebuilt from scratch.

From reading to strategy

Why finance should guide strategy, not just reporting argues the P&L should change decisions: pricing, hiring freeze, product kill, market exit. Why every business needs CFO thinking for smarter growth is the ownership model — someone turns P&L variance into action.

Build KPIs that trace to P&L lines — revenue growth, gross margin %, opex as % of revenue, customer acquisition cost payback where measurable. How to create financial KPIs for your company closes the loop.

Tools and automation

Modern ledgers produce P&L on demand — if coding is clean. AI in accounting for UAE businesses helps flag miscoded blocks and anomalies before month-end close. Automation does not replace the variance narrative — that remains human judgment tied to operations.

Worked example — reading variance in plain language

Suppose revenue rose 12% month-on-month but gross margin fell from 46% to 41%. A useful narrative:

- Mix: lower-margin product line grew from 30% to 45% of revenue.

- Price: one enterprise client received a 5% renewal discount.

- Cost: freight on imports rose; not yet passed through to pricing.

- Action: pricing committee in two weeks; temporary margin floor on discounts; freight surcharge review with ops.

That paragraph changes behaviour. A slide that says “margin down 5 pts” without causation does not. Train leadership to expect narratives — not only numbers — from finance.

Board and investor packs — P&L presentation tips

External audiences want:

- Recurring vs non-recurring split clearly labelled.

- EBITDA bridge if you use the term — with consistent add-backs documented.

- Cash conversion comment — even one sentence linking to cash flow.

- Same definitions as prior periods — restate if you change coding.

How to build an investor-ready financial story in the UAE starts with P&L integrity. Build financial systems before scaling ensures the pack is exportable from the ledger, not rebuilt in PowerPoint under deadline pressure.

The bottom line

Learning how to read a profit and loss statement means reading gross margin first, explaining variances in plain language, separating recurring from one-off, and pairing profit with cash every month. The P&L tells you whether the model works; it does not tell you whether you can pay next month’s payroll without the cash flow statement and balance sheet beside it.

Train your leadership team to ask “what changed gross margin?” before “what changed revenue?” — that single habit catches pricing and delivery problems earlier than top-line celebrations. Over time, pair P&L review with how to create financial KPIs for your company so the same definitions appear in dashboards, board packs, and tax working papers — one truth, many uses.

When you present externally, reconcile net profit to the narrative you use for valuation or fundraising — increase business valuation strategies and investor pitch deck mistakes founders make both assume the P&L in the room matches the P&L in the system.

Schedule a fixed monthly P&L review on the calendar — same day each month after close — so reading the statement becomes habit rather than a crisis response to a bank or investor request. Habits beat heroics; the founders who read margin first rarely need emergency restructuring later.

Browse the Finance desk or book a free consultation if you want help structuring management accounts for your entity.

This article is general information for UAE-based businesses and is not legal, tax, or financial advice. Confirm your specific reporting obligations with a qualified adviser.

Questions and answers

What is the difference between profit and cash on a P&L?

The P&L records revenue when earned and expenses when incurred under accrual accounting — regardless of when cash moves. You can show profit while cash falls if customers pay late, you prepay costs, or you invest in inventory. That is why founders must read how to read a cash flow statement alongside the P&L every month.

Which P&L lines should founders review first?

Start with revenue by major stream, gross profit and gross margin percentage, then the largest operating expense categories — typically people, marketing, and rent. Scan net profit last; the story usually lives in margin and opex discipline before tax and one-offs distort the bottom line.

How often should a UAE SME review its P&L?

Monthly at minimum, closed within 5–10 business days of month-end. High-growth or tight-cash businesses benefit from weekly flash reports on revenue and gross margin, with full P&L monthly. Quarterly alone is too slow when payroll and marketing burn are fixed.

What is EBITDA and should SMEs care?

EBITDA is earnings before interest, tax, depreciation, and amortisation — a rough proxy for operating cash generation before capital structure and non-cash charges. Investors use it; operators should understand it but not worship it. Capital-heavy businesses can show strong EBITDA while still needing cash for assets and debt service.

Why does my P&L not match my bank balance?

Timing differences: unpaid invoices inflate revenue vs cash, prepaid expenses hit cash before the P&L, loan principal does not appear in P&L, VAT collected sits as liability on the balance sheet. Reconcile deliberately — mismatch is normal; unexplained mismatch is a control problem.

More in Finance

View all Finance →

What UAE Businesses Should Expect From Annual Accounting Services

Annual accounting services should provide reliable year-end records, financial statements, tax preparation support, reconciliations, and practical financial insight. This UAE guide explains reasonable expectations, common exclusions, and how to prepare.

How Long Does It Take to Adjust Financialladjust-financially-moving-dubai

Most newcomers need three to six months to adjust financially after moving to Dubai. Housing, relocation costs, family size and lifestyle choices can make the process shorter or longer.

What's the Real Cost of Dining Out and Entertainment in Dubai in 2026?

A practical 2026 guide to dining, nightlife and entertainment costs in Dubai, with realistic budget ranges, hidden expenses and money-saving advice for visitors, residents and business professionals.