How to Read a Cash Flow Statement

Profit is an opinion; cash is a fact. Here is how UAE founders and operators read a cash flow statement — operating, investing, and financing activities — to survive growth, tax, and payroll without surprises.

Key takeaways

- The cash flow statement explains how cash moved in a period — separate from profit on the P&L and balances on the balance sheet.

- Operating cash flow is the core health signal: can the business generate cash from normal activities without relying on new debt or equity?

- Growth often shows profit while operating cash falls — receivables, inventory, and prepayments absorb cash before leadership notices.

- Investing and financing sections reveal capex, acquisitions, loan draws, repayments, and distributions — strategic choices with liquidity impact.

- Founders should reconcile profit to operating cash monthly and maintain a rolling cash forecast — the statement explains history; the forecast protects the future.

Revenue charts go up and to the right on every deck. Payroll still clears on a Thursday. When those two facts collide, founders discover — often too late — that profit and cash are not the same thing. The cash flow statement exists to make that gap visible: where cash came from, where it went, and whether the business can fund itself from operations or depends on borrowing, investment, or founder subsidies.

This guide explains how to read a cash flow statement as a UAE operator: the three sections, the reconciliation from profit to operating cash, the patterns that predict trouble during growth, and how to pair historical statements with forward forecasts. If you read nothing else on finance this quarter, read this alongside why cash flow matters more than growth claims in UAE business.

Three statements — one story

| Statement | Question | |-----------|----------| | P&L | Did we perform? (how to read a profit and loss statement) | | Balance sheet | What do we own and owe? (how to read a balance sheet like a business owner) | | Cash flow | What moved in the bank? |

Why accounting is business intelligence for UAE businesses only works when all three are read together monthly.

Profit measures performance over time. Cash measures survival today. Growth punishes founders who confuse them.

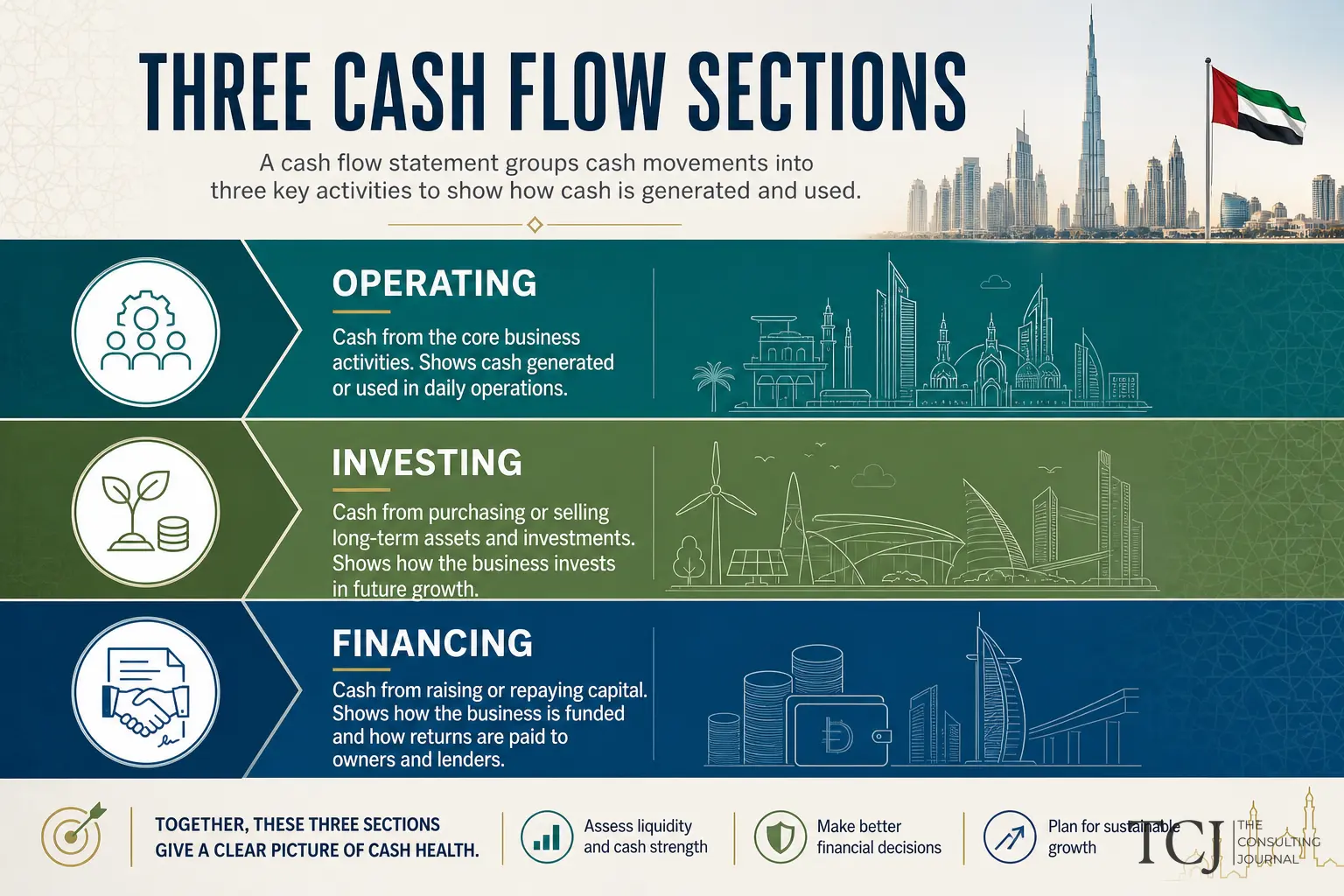

Structure of the cash flow statement

Standard presentation divides cash movement into three blocks:

1. Operating activities

Cash from running the business — collections from customers, payments to suppliers and staff, rent, tax paid, interest paid (classification can vary by standard — stay consistent with your accountant).

Indirect method (common): starts with net profit, adds back non-cash charges (depreciation), adjusts for changes in working capital:

- AR increase — cash unfavourable (you recognised revenue not yet collected).

- Inventory increase — cash unfavourable (you bought stock).

- AP increase — cash favourable (you delayed supplier payment).

- Deferred revenue increase — cash favourable (customer paid ahead).

This reconciliation is where why businesses fail during growth phases becomes visible — profit up, operating cash down, month after month.

2. Investing activities

Cash used for or from long-term assets and investments:

- Purchase or sale of equipment, vehicles, fit-out.

- Software capitalised or acquired.

- Acquisitions or divestments.

- Deposits and investments.

Capex-heavy months can look “bad” on cash while strategically necessary — the question is whether returns are modelled, not whether the line is negative.

3. Financing activities

Cash from or to capital providers:

- Loan drawdowns and repayments.

- Equity injections.

- Dividends or distributions.

- Lease principal payments (where classified here).

Repeated reliance on financing cash to cover weak operating cash is a structural warning — not a one-month blip.

How to read operating cash — the priority section

Step 1 — Compare to net profit

If net profit is positive and operating cash is negative repeatedly:

- Check AR ageing — collection failure or aggressive revenue recognition.

- Check inventory build — trading businesses especially.

- Check prepaid spikes — marketing, rent, suppliers.

- Check tax/VAT payments vs P&L accrual — how to plan taxes before year-end includes cash provisioning for this reason.

Step 2 — Trend three to six months

One month can distort — large supplier payment, VAT quarter, bonus payout. Trend operating cash vs profit; widening gap needs a written explanation in leadership notes.

Step 3 — Link to KPIs

Cash conversion metrics belong in how to create financial KPIs for your company: DSO, DPO, cash runway, operating cash margin where applicable.

Investing cash — growth vs maintenance

Separate:

- Maintenance capex — replace laptops, refurbish office, keep lights on.

- Growth capex — new line, warehouse, major software implementation.

Build financial systems before scaling and how to choose accounting software for your business often appear here as implementation spend — budget before you sign.

Negative investing cash is normal for growing asset bases; unexplained negative investing without board awareness is not.

Financing cash — know your dependencies

Patterns:

- Operating weak, financing positive — borrowing or equity funding the gap. Temporary bridge or chronic model issue?

- Operating strong, financing negative — repaying debt or distributing cash — healthy if intentional.

- Founder loans in/out — document terms; due diligence will ask.

What investors check before funding a business includes how often you return to the well for cash without fixing conversion.

UAE-specific cash considerations

VAT — quarterly or monthly payments can create lumpy outflows; model separately from operating opex. Keeping UAE accounting records ready for tax filing and audit keeps payable balances reconciled.

Corporate tax — cash payment dates differ from provision on P&L; provision early per corporate tax mistakes to avoid in 2026.

Payroll and WPS — fixed calendar outflows; growth hiring increases immovable cash need before revenue catches up.

Banking — why every business needs CFO thinking for smarter growth includes treasury: which account holds tax cash, which holds operating, who initiates transfers — controls matter when volume rises.

From statement to forecast — protect next quarter

Historical cash flow explains the past. Operators survive on forward visibility:

- Rolling thirteen-week forecast — updated weekly.

- Categories: payroll, rent, suppliers, tax, debt service, capex, discretionary.

- Scenarios: base, conservative, stress (AR slips two weeks).

How to build a practical business budget feeds the forecast; variance analysis feeds back to the budget.

Monthly financial reports every founder should review in the UAE should include cash summary even when full statutory cash flow statement is accountant-prepared quarterly.

Monthly cash review agenda (twenty minutes)

- Opening and closing cash vs forecast.

- Operating cash vs net profit — bridge explained.

- Largest unexpected outflows — one-off or recurring?

- AR and AP movement vs balance sheet.

- Next ninety days tax, payroll, and debt events.

- Runway at current burn — hire/pause decision input.

Outsourced CFO services in the UAE often own this cadence when founders lack time — but leadership must still read the output.

Direct method vs indirect — what founders see

Many SME packs use the indirect method — start from profit, adjust non-cash and working capital. Some operators prefer a direct method summary: cash from customers minus cash to suppliers and staff. You do not need both in statutory format, but leadership may understand direct summaries faster in early stages. Pick one internal format and reconcile to the ledger monthly — consistency beats sophistication.

Systems, registration, and cash timing

Informal finance during early growth produces cash surprises at registration milestones. Why small businesses need systems early reduces the gap between when VAT or corporate tax obligations begin and when cash processes catch up. Corporate tax registration is done: what UAE businesses should do next and VAT registration in the UAE: when your business should act both shift cash outflows onto a calendar — model them in forecast, not only in P&L tax lines.

Tax planning vs tax avoidance for UAE business owners applies to cash timing: legitimate planning provisions cash; schemes that defer recognition without substance create statement noise and diligence risk.

Valuation and exit — cash quality premium

Buyers pay for sustainable cash conversion, not peak EBITDA. Increase business valuation strategies assume you can show operating cash trend alongside profit — weak conversion caps multiples even in hot markets. Build the bridge narrative before a process starts, not during exclusivity when buyers pressure price.

Common cash flow mistakes

- Managing from bank balance alone — no bridge from profit; surprises stay mysterious.

- Ignoring working capital — growth consumes cash silently.

- VAT and tax as afterthought — lumpy hits without provision account.

- Capitalising opex to flatter profit — operating cash still leaves.

- Confusing financing inflow with revenue — runway illusion.

- No forecast — reactive firefighting every payroll week.

Investor pitch deck mistakes founders make include cash slides that ignore working capital and tax timing.

Cash flow and strategy

Why finance should guide strategy, not just reporting uses cash facts for pricing (deposits, milestones), customer terms (reduce DSO), supplier terms (extend DPO ethically), and hire timing.

Why revenue alone does not impress investors — cash quality completes the argument.

How to build an investor-ready financial story in the UAE requires three-way models — P&L, balance sheet, cash — that reconcile.

Automation and the future

AI in accounting for UAE businesses improves categorisation and anomaly detection on bank feeds — faster reconciliation into cash analysis. The future of finance is advisory, automation, and control describes real-time cash views becoming standard — but forecasts and decisions remain human-owned.

Small business relief and corporate tax affect cash tax outflows — model elections with your accountant, not only P&L impact.

Worked bridge — profit to operating cash (conceptual)

Net profit AED 200,000 for the month.

Add back depreciation AED 30,000 (non-cash).

Working capital changes:

- AR increased AED 80,000 → cash unfavourable.

- Inventory increased AED 40,000 → cash unfavourable.

- AP increased AED 25,000 → cash favourable.

Approximate operating cash ≈ 200 + 30 − 80 − 40 + 25 = AED 135,000 — still positive, but materially below profit. That gap is the conversation leadership needs — not celebration on profit alone.

Repeat this bridge monthly until reading it becomes reflex — the skill why finance should guide strategy, not just reporting depends on.

Treasury hygiene alongside the statement

Separate operating cash from tax-provision cash mentally even if accounts sit in one bank. Founders who commingle spend tax money on opex and discover the gap at filing — corporate tax in UAE mistakes businesses must avoid in 2026 documents the pattern. Cash flow statement plus treasury rules prevents it.

Review who can initiate transfers — growth increases fraud and error surface. Build financial systems before scaling includes treasury policy as a control layer, not only accounting policy.

Free cash flow — the investor lens

Free cash flow approximates cash available after operating needs and maintenance capex — often operating cash minus sustaining capital expenditure. Growth capex may sit outside that definition depending on who you ask — document your convention and stay consistent.

Investors compare free cash flow to net profit over trailing periods — persistent gaps signal working capital drag or capex underinvestment. What investors check before funding a business includes that comparison; build the bridge internally before they ask.

For owner-operators, free cash flow answers “what could we distribute, reinvest, or use to pay down debt this year?” — without confusing paper profit with available cash.

Cash flow and hiring decisions

Before approving a hire class, model incremental cash out — salary, visa, benefits, equipment — against expected cash in timing from revenue drivers. The cash flow statement historical pattern informs realistic collection assumptions; the forecast applies them forward.

If operating cash is weak three months running, hiring without changing collection or terms is a bet — make it explicitly, not accidentally. Why every business needs CFO thinking for smarter growth is the ownership frame for that conversation.

Subscription and milestone businesses — cash flow patterns

Subscription models show deferred revenue on the balance sheet — cash collected upfront, revenue recognised over time. Operating cash can look strong while P&L revenue lags billings — or the reverse if churn rises and new sales slow. Read deferred revenue balance trend alongside MRR or contract backlog.

Project and milestone businesses show the opposite timing risk: revenue recognised at milestone while costs were incurred earlier — profit spikes do not equal cash until invoicing and collection complete. Map milestone billing to delivery calendar in forecast, not only in project management tools disconnected from finance.

Both patterns explain why how to read a profit and loss statement and how to read a balance sheet like a business owner must accompany cash flow review — no single statement tells the full story. Treat the three as one monthly ritual, not three optional reports.

The bottom line

Learning how to read a cash flow statement means prioritising operating cash, reconciling profit to cash every month, understanding investing and financing choices, and pairing history with a rolling forecast. The statement explains where cash went; your job is to ensure next month’s payroll, VAT, and growth commitments are funded deliberately — not accidentally.

Profit is the story you tell. Cash is the story that must be true.

Operators who master both statements — and the balance sheet between them — make fewer survival mistakes during growth. Revisit this guide monthly until the three-statement read takes less than forty-five minutes combined; speed comes from familiarity, not from skipping sections.

Browse the Finance desk or book a free consultation for help building cash packs and forecasts for your entity.

This article is general information for UAE-based businesses and is not legal, tax, or financial advice. Confirm your specific obligations with a qualified adviser.

Questions and answers

Why is my business profitable but cash flow negative?

Common bridges: customers have not paid (AR up), you bought inventory ahead of sales, you prepaid expenses, you paid down payables, VAT or tax payments exceeded P&L charge, or you invested in capex. The cash flow statement lists these adjustments explicitly — read operating activities before panicking about net profit.

What is operating cash flow?

Cash generated or used by core business operations — typically starting from net profit and adjusting for non-cash items (depreciation) and working capital changes (AR, inventory, AP). Strong operating cash flow means the model throws off cash; weak or negative operating cash during stable operations is a warning even if profit is positive.

Do small UAE businesses need a formal cash flow statement?

Statutory requirements depend on entity size and standards applied — your accountant advises. Operationally, every founder needs cash flow visibility regardless of format: direct method summary or indirect statement from the ledger, plus a forward forecast. Monthly financial reports every founder should review in the UAE treats cash as non-negotiable.

How is a cash flow forecast different from the cash flow statement?

The statement is historical — what happened. The forecast is forward — expected inflows and outflows, usually weekly or thirteen-week rolling. Both matter: the statement explains variances; the forecast prevents payroll and tax surprises. Pair with why cash flow matters more than growth claims in UAE business.

What cash flow metrics do investors watch?

Operating cash flow trend, free cash flow after capex, cash conversion of EBITDA, working capital days, and runway at current burn. What investors check before funding a business and why revenue alone does not impress investors both emphasise cash quality over headline growth.

More in Finance

View all Finance →

What UAE Businesses Should Expect From Annual Accounting Services

Annual accounting services should provide reliable year-end records, financial statements, tax preparation support, reconciliations, and practical financial insight. This UAE guide explains reasonable expectations, common exclusions, and how to prepare.

How Long Does It Take to Adjust Financialladjust-financially-moving-dubai

Most newcomers need three to six months to adjust financially after moving to Dubai. Housing, relocation costs, family size and lifestyle choices can make the process shorter or longer.

What's the Real Cost of Dining Out and Entertainment in Dubai in 2026?

A practical 2026 guide to dining, nightlife and entertainment costs in Dubai, with realistic budget ranges, hidden expenses and money-saving advice for visitors, residents and business professionals.