How to Read a Balance Sheet Like a Business Owner

Assets, liabilities, and equity tell you what the business owns, owes, and whether growth is funded sustainably. Here is how UAE founders read a balance sheet for liquidity, leverage, and working capital — without an accounting degree.

Key takeaways

- The balance sheet is a snapshot at a date — it shows what you own, what you owe, and what is left for owners; it complements the P&L and cash flow statement, it does not replace them.

- Working capital — current assets minus current liabilities — drives day-to-day survival; growth into inventory or long payment terms loads the balance sheet even when the P&L looks fine.

- Debt and lease commitments live on the balance sheet; founders who only watch revenue miss covenant and liquidity risk until banking conversations turn painful.

- Equity is not cash — retained profit increases equity but may sit in receivables or stock; understand where value is trapped.

- Review the balance sheet monthly once you have material AR, inventory, debt, or deferred revenue — not only at year-end.

Founders live in revenue. Operators live in margin. Surviving growth requires a third lens: what the business owns and owes right now. That is the balance sheet — a snapshot at a date, not a movie like the P&L. Ignore it and you can hit payroll while showing profit, breach loan covenants while celebrating pipeline, or walk into investor due diligence with receivables that do not convert.

This guide explains how to read a balance sheet like a business owner: the sections that matter, the ratios worth tracking without a finance team, and how the balance sheet connects to cash and strategy in UAE businesses. Read it alongside how to read a profit and loss statement and how to read a cash flow statement — three statements, one story.

Snapshot vs period — mindset first

The balance sheet answers at one date (month-end, year-end):

- What do we own (assets)?

- What do we owe (liabilities)?

- What is left for owners (equity)?

The P&L covers a period — a month or year of performance. Cash flow explains movement of cash over a period. Together:

- P&L → did the model work?

- Balance sheet → what accumulated?

- Cash flow → what actually moved in the bank?

Equity is not spending money. Cash is. Retained profit on the balance sheet may sit in invoices customers have not paid.

Why accounting is business intelligence for UAE businesses applies to all three — not only revenue.

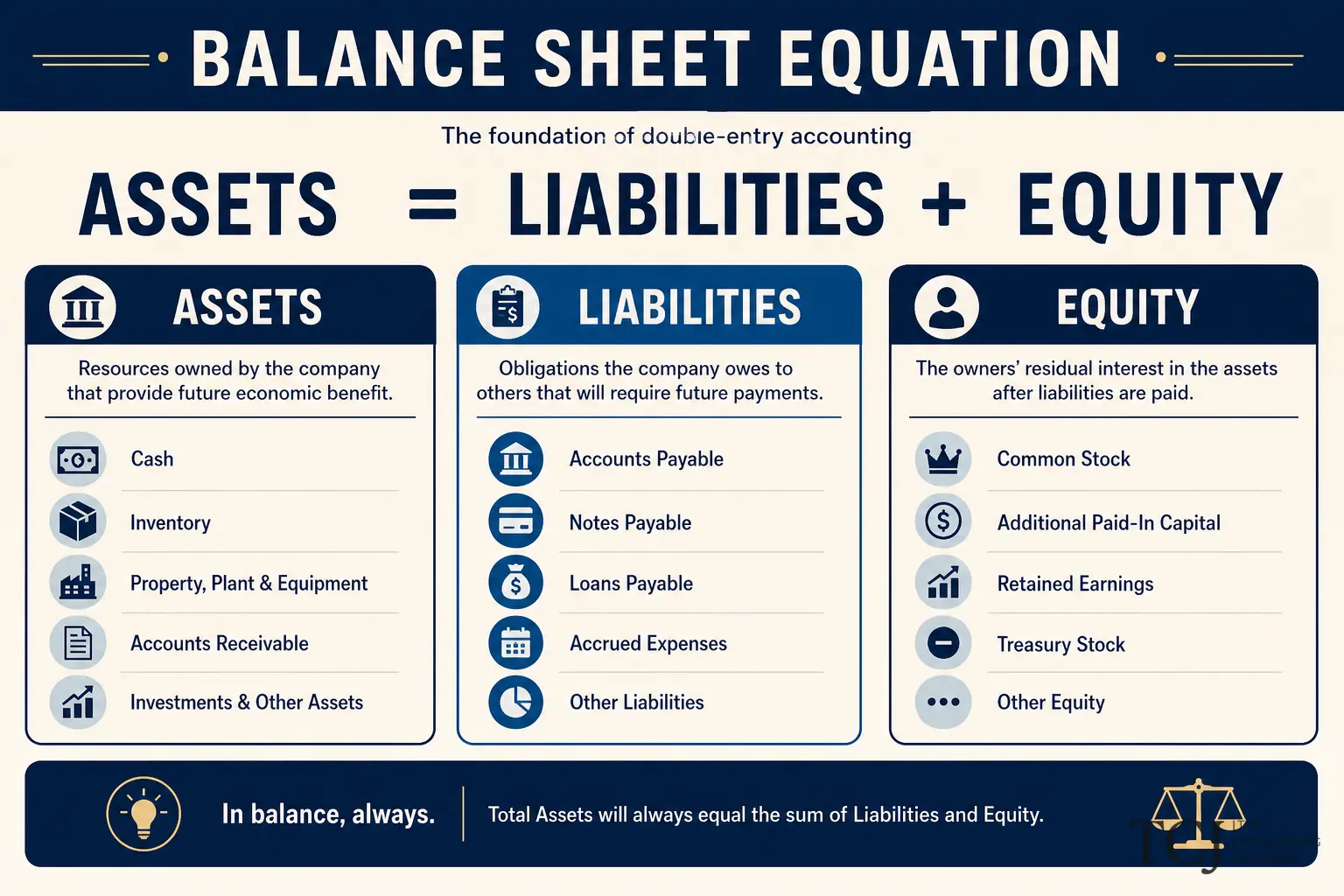

Assets — where value sits (and gets stuck)

Current assets (roughly ≤ 12 months)

Cash and bank — liquid; separate operating from tax-provision balances mentally per how to plan taxes before year-end.

Accounts receivable (AR) — customers owe you. Review ageing weekly during growth; AR rising faster than revenue is a collection or quality problem. Pair with monthly financial reports every founder should review in the UAE.

Inventory — goods for sale or materials. Trading and retail businesses: count, ageing, obsolescence. Miscoded inventory distorts COGS on the P&L — see how to read a profit and loss statement.

Prepayments — rent, insurance, suppliers paid ahead. Cash out already; benefit spreads on P&L later.

VAT recoverable — input tax awaiting refund or offset; track against filings per keeping UAE accounting records ready for tax filing and audit.

Non-current assets

Property, plant, equipment (PPE) — at cost less depreciation. Capex decisions live here — not in day-to-day opex unless incorrectly capitalised.

Intangibles — software capitalised, acquisitions, licences. Due diligence asks how these were valued.

Investments and deposits — long-term security deposits, related-party loans given.

Founder question: Is growth funding more current assets (working capital) or capex (long-term bets)? Each needs different cash planning.

Liabilities — what you owe and when

Current liabilities

Accounts payable (AP) — you owe suppliers. Stretching AP is free financing until it damages relationships or terms.

Accrued expenses — wages, bonuses, utilities incurred not yet paid. Year-end accrual discipline matters for tax and truth.

Deferred revenue / customer deposits — cash received, service not yet delivered. Common in subscriptions and projects; affects when revenue hits P&L.

VAT payable — collected tax owed to FTA; not your money — treat as restricted cash mentally.

Short-term debt and current portion of long-term debt — what must refinance or repay within a year. Covenant tests often tie here.

Non-current liabilities

Long-term loans — bank facilities, founder loans with terms, related-party debt.

Lease liabilities — where applicable under accounting standards; affects leverage ratios.

Provisions — warranties, legal, restructuring if recognised.

Founder question: What is due in the next ninety days vs comfortably distant? Banks care about the near term.

Equity — owners’ stake

Share capital — paid-in by shareholders.

Retained earnings — accumulated profit less dividends/distributions. Can be large while cash is low if profit sits in AR or inventory.

Current year profit — sometimes shown separately until year-end close.

Negative equity — liabilities exceed assets — is a solvency warning even if operations feel “fine” day to day. Do not ignore because the P&L is positive this month.

Working capital — the operator’s core metric

Working capital = Current assets − Current liabilities

Current ratio = Current assets ÷ Current liabilities (aim for context-appropriate levels — not one magic number)

Quick ratio — excludes inventory from current assets; harsher liquidity test for traders.

During growth, working capital consumes cash when:

- You stock inventory before sales season.

- Customers pay in sixty days; you pay payroll in thirty.

- Projects require WIP buildup before milestone billing.

Why cash flow matters more than growth claims in UAE business is the narrative; working capital is often the mechanism.

Track days sales outstanding (DSO), days inventory outstanding (DIO), days payables outstanding (DPO) — simple averages linking balance sheet to operations. How to create financial KPIs for your company includes these in a starter dashboard.

Debt and leverage — read before you borrow more

Key questions:

- Total debt vs equity — debt-to-equity trend.

- Interest coverage — EBIT vs interest (from P&L + balance sheet).

- Covenant headroom on facilities — often in loan docs founders never opened.

- Related-party loans — documented terms? Arm’s length?

What investors check before funding a business and how to build an investor-ready financial story in the UAE assume leverage is explainable — not buried in “other payables.”

How to read a balance sheet in twenty minutes monthly

- Cash — trend vs last month; vs forecast.

- AR ageing — total and >60 days bucket.

- Inventory — level vs sales; any obsolescence flag.

- AP — overdue vs strategic stretch.

- Deferred revenue — obligation to deliver; matches pipeline?

- Debt — next maturity; covenant notes.

- Equity — retained earnings vs cash reality; any distributions planned?

Write three bullets: liquidity, working capital pressure, leverage or equity movement.

Compare to how to build a practical business budget — balance sheet is where budget assumptions land in reality.

Balance sheet and UAE tax/compliance

VAT — recoverable and payable balances should reconcile to returns. Misstatement here flows to cash and compliance risk — VAT registration in the UAE is entry; ongoing reconciliation is discipline.

Corporate tax — deferred tax assets/liabilities may appear for larger entities; SMEs still need provisions and documented estimates per corporate tax registration done: next steps and corporate tax mistakes to avoid in 2026.

Related-party balances — due to/from group companies need agreements and disclosure support — tax planning vs tax avoidance stresses substance.

Early-stage balance sheet — when it starts to matter

Even lean services businesses should watch the balance sheet once AR, deferred revenue, or director loans appear. Why small businesses need systems early prevents informal related-party balances from becoming due-diligence problems — “founder loan” without terms is common and fixable early, embarrassing late.

When revenue quality matters for external capital, balance sheet composition supports P&L narrative — why revenue alone does not impress investors pairs with receivables quality and deferred revenue obligations on the balance sheet.

Relief, provisions, and equity impact

Corporate tax and relief elections affect retained earnings and cash separately. Small business relief in UAE corporate tax may reduce tax expense in P&L when eligible — but eligibility evidence lives in documentation, not hope. Watch equity grow from paper profit while cash stagnates in AR; that pattern is visible only on the balance sheet alongside how to read a cash flow statement.

Common balance sheet blind spots

- Founder loans informally tracked — no terms, no repayment schedule.

- Personal assets mixed in — distorts every ratio.

- Stale inventory at inflated values — overstates equity until write-down.

- Unbilled revenue or WIP without substantiation — optimism on assets.

- Off-balance commitments — personal guarantees, pending litigation, LOIs ignored.

- Only reading P&L — classic growth-phase failure per why businesses fail during growth phases.

Balance sheet drives strategy

Why finance should guide strategy, not just reporting uses balance sheet facts for:

- Hire or hold — cash and runway after working capital needs.

- Stock up or stay lean — inventory policy vs DIO.

- Terms negotiation — customer deposits, milestone billing to reduce AR drag.

- Fundraise timing — equity before covenants bite or AR quality degrades.

Why every business needs CFO thinking for smarter growth and outsourced CFO services in the UAE help when these decisions exceed founder bandwidth.

Systems that keep the balance sheet honest

Build financial systems before scaling includes monthly close, reconciliations, and document storage. How to choose accounting software for your business should support aged reports, inventory modules if needed, and bank rec — not only P&L buttons.

AI in accounting for UAE businesses flags reconciliation breaks and duplicate vendors — balance sheet hygiene at speed.

Valuation and exit context

Buyers price off earnings and balance sheet quality — normalized working capital, debt-free/cash-free adjustments, quality of earnings on receivables and inventory. Increase business valuation strategies assumes defensible statements — not year-end heroics.

Investor pitch deck mistakes founders make include showing revenue charts without working capital or cash narrative.

Worked ratios — quick mental math for owners

Current ratio example: Current assets AED 800,000; current liabilities AED 500,000 → ratio 1.6. Context matters — a services firm may run fine at 1.2; a trader with fast inventory turnover may need higher. Track trend, not absolutes.

Debt-to-equity example: Total debt AED 1,200,000; equity AED 800,000 → 1.5x leverage. Rising leverage during flat cash conversion is a warning — especially before what investors check before funding a business reviews capital structure.

Working capital days: Link balance sheet to operations via DSO + DIO − DPO — covered in how to create financial KPIs for your company. Balance sheet snapshots feed those KPIs; review together monthly.

Seasonality and UAE business cycles

Retail, events, and tourism-linked businesses see predictable seasonal balance sheet swings — inventory build before peak, AR spike after. Compare same month prior year, not only prior month, to avoid misreading normal seasonality as crisis. Budget seasonality explicitly in how to build a practical business budget so leadership expects working capital absorption in advance.

Intercompany and group balances — SME reality

Even small groups accumulate due-to/due-from balances between entities — management charges, shared rent, loan balances. Each should have written terms, repayment expectation, and reconciliation schedule. Founders treat intercompany as “internal” until due diligence or tax review treats it as material related-party exposure.

Monthly group review should confirm balances tie across entities — mismatches signal coding errors or missing invoices that compound silently. Outsourced CFO services in the UAE often maintain simple group reconciliation packs before full consolidation software is justified.

Inventory and WIP — balance sheet items that move P&L

Trading and project businesses: inventory and work-in-progress are balance sheet assets until sold or billed. Miscounts inflate assets and understate COGS — flattering both balance sheet equity and P&L margin until adjustment. Count discipline is not warehouse bureaucracy; it is financial truth.

Align count frequency with business velocity — monthly minimum for material stock; weekly during peak. Tie results to how to read a profit and loss statement COGS line explanations when margin shifts.

Debt covenants — read the documents

If you have bank facilities, locate covenant definitions — they may use adjusted EBITDA, minimum liquidity, or AR caps different from your internal KPIs. Finance should translate covenants into monthly dashboard lines before breach, not after the relationship manager calls.

Covenant headroom belongs in the same meeting as cash runway — why cash flow matters more than growth claims in UAE business applies when debt service is in the forecast.

The bottom line

Reading a balance sheet like a business owner means tracking where value sits, what is owed and when, and whether growth is funded sustainably — not obsessing over a single ratio in isolation. Review cash, receivables, inventory, payables, deferred revenue, and debt monthly once working capital matters. Pair the snapshot with P&L performance and cash flow movement.

The balance sheet warns before the P&L screams. Use it monthly once working capital, debt, or deferred revenue matter — and connect every snapshot to the cash flow story that follows.

If you operate across multiple contracts or payment terms, build a simple liquidity calendar beside the balance sheet: when large receivables are due, when VAT and corporate tax cash out, when loan repayments hit — the calendar turns static balances into actionable timing. That habit bridges how to read a cash flow statement and how to plan taxes before year-end without waiting for month-end surprise.

Review equity and debt together once per quarter — leverage trends matter as much as monthly cash for long-term solvency.

Browse the Finance desk or book a free consultation for help structuring monthly packs for your entity.

This article is general information for UAE-based businesses and is not legal, tax, or financial advice. Confirm your specific obligations with a qualified adviser.

Questions and answers

What is the accounting equation on a balance sheet?

Assets = Liabilities + Equity. Everything the business owns (assets) is funded either by creditors (liabilities) or owners (equity). If the equation does not balance, there is an error in the books — full stop. Every month-end close should produce a balanced trial balance and balance sheet.

Why should founders care about the balance sheet if the P&L shows profit?

Profit can rise while cash is trapped in receivables or inventory, or while debt funds the gap. The balance sheet reveals liquidity, leverage, and working capital pressure that the P&L hides. During growth, why businesses fail during growth phases often involves balance sheet strain despite positive profit.

What are current vs non-current assets and liabilities?

Current items are generally expected to convert to cash or settle within twelve months — cash, receivables, inventory, payables, short-term debt. Non-current items are longer-term — property, equipment, long-term loans, deferred tax. Liquidity analysis focuses on the current section first.

How often should a UAE SME review its balance sheet?

Monthly alongside the P&L once you have meaningful working capital — typically when AR, inventory, or payables exceed a few weeks of operating cost. Pure services micro-businesses may start quarterly, but should move to monthly before fundraising, bank facilities, or rapid hiring.

What balance sheet red flags do investors notice?

Rising receivables faster than revenue, inventory ageing without write-down, related-party balances without documentation, negative equity, hidden contingent liabilities, large unexplained 'other' lines, and mismatches between cash and retained earnings growth. What investors check before funding a business treats the balance sheet as due-diligence core.

More in Finance

View all Finance →

What UAE Businesses Should Expect From Annual Accounting Services

Annual accounting services should provide reliable year-end records, financial statements, tax preparation support, reconciliations, and practical financial insight. This UAE guide explains reasonable expectations, common exclusions, and how to prepare.

How Long Does It Take to Adjust Financialladjust-financially-moving-dubai

Most newcomers need three to six months to adjust financially after moving to Dubai. Housing, relocation costs, family size and lifestyle choices can make the process shorter or longer.

What's the Real Cost of Dining Out and Entertainment in Dubai in 2026?

A practical 2026 guide to dining, nightlife and entertainment costs in Dubai, with realistic budget ranges, hidden expenses and money-saving advice for visitors, residents and business professionals.